Save more, spend smarter, and make your money go further

Buying your first home? An FHA loan might be the answer to financing your purchase.

What is an FHA loan? An FHA loan is a mortgage that’s insured by the Federal Housing Administration (FHA), which allows lower qualifications for the borrower than the norm. They’re most popular for first-time home buyers since the down payment can be as low as 3.5%, while some types of mortgage loans require 20-30%.

If you’re weighing your loan options, learn more about the FHA loan requirements, along with the pros and cons, to determine if it’s the right fit for you.

What Is an FHA Loan?

An FHA loan is a type of mortgage that’s insured by the Federal Housing Administration. FHA loans have more flexible credit score and down payment requirements than conventional loans, making them popular among first-time home buyers.

What Is an FHA Loan?

An FHA loan is a loan offered by the U.S. Federal Housing Administration, which means it’s backed by the government. When you apply for an FHA loan, you can get more favorable loan terms, which means you can create a budget that’s easier for you and your family to stick to.

FHA loans can potentially be a good way for homeowners who don’t have the best credit score to get approved for a mortgage loan. However, it’s important to keep in mind that there are key differences between FHA home loans and conventional mortgage loans.

What Are the Requirements for an FHA Loan?

An FHA mortgage makes becoming a homeowner feasible for people of all income levels since the government is guaranteeing the payment of your loan. Unlike most mortgage loans, there is no minimum income required to qualify for an FHA loan, but you do need to show that you can repay the loan. Take a look at our complete guide to all FHA loan requirements:

Credit score. Your credit score factors into the percentage of down payment you put on the house. If you have a credit score of 580 or higher, you pay a 3.5% down payment, but if you have a credit score lower than 580, you pay a 10% down payment.

Employment history. You must demonstrate a steady employment history or have worked at the same employer for the past two years.

Legality. You must have a Social Security number, be a resident of the U.S. and be of legal age to sign a mortgage.

Income ratio. This is dependent on your lender, but typically your mortgage payment — including HOA fees, property taxes, mortgage insurance and homeowners insurance — needs to be less than 31% of your gross income. Additionally, your mortgage including your monthly debt needs to be less than 43% of your gross income. You can use a budgeting calculator to figure out if you’re ready to buy a home.

Bankruptcy background. You should be at least two years out of bankruptcy and have re-established good credit, but some lenders may make exceptions.

Foreclosure background. You should be at least three years out of foreclosure and have re-established good credit, but similar to your bankruptcy background, some lenders may make exceptions.

Private lenders, whether a bank or credit union, may have stricter qualifications than the FHA requirements, so it’s recommended to check with a variety of lenders before making your final decision.

How Does an FHA Loan Work?

The requirements to qualify for an FHA loan may sound too good to be true, but it’s all made possible through one thing: mortgage insurance.

Private lenders issue the loan for your home, but the FHA provides the backing for part of the loan, so if you don’t repay your loan, the FHA will pay the lender instead. This provides the lender with the reassurance that your loan will be repaid, thus providing you with a better deal.

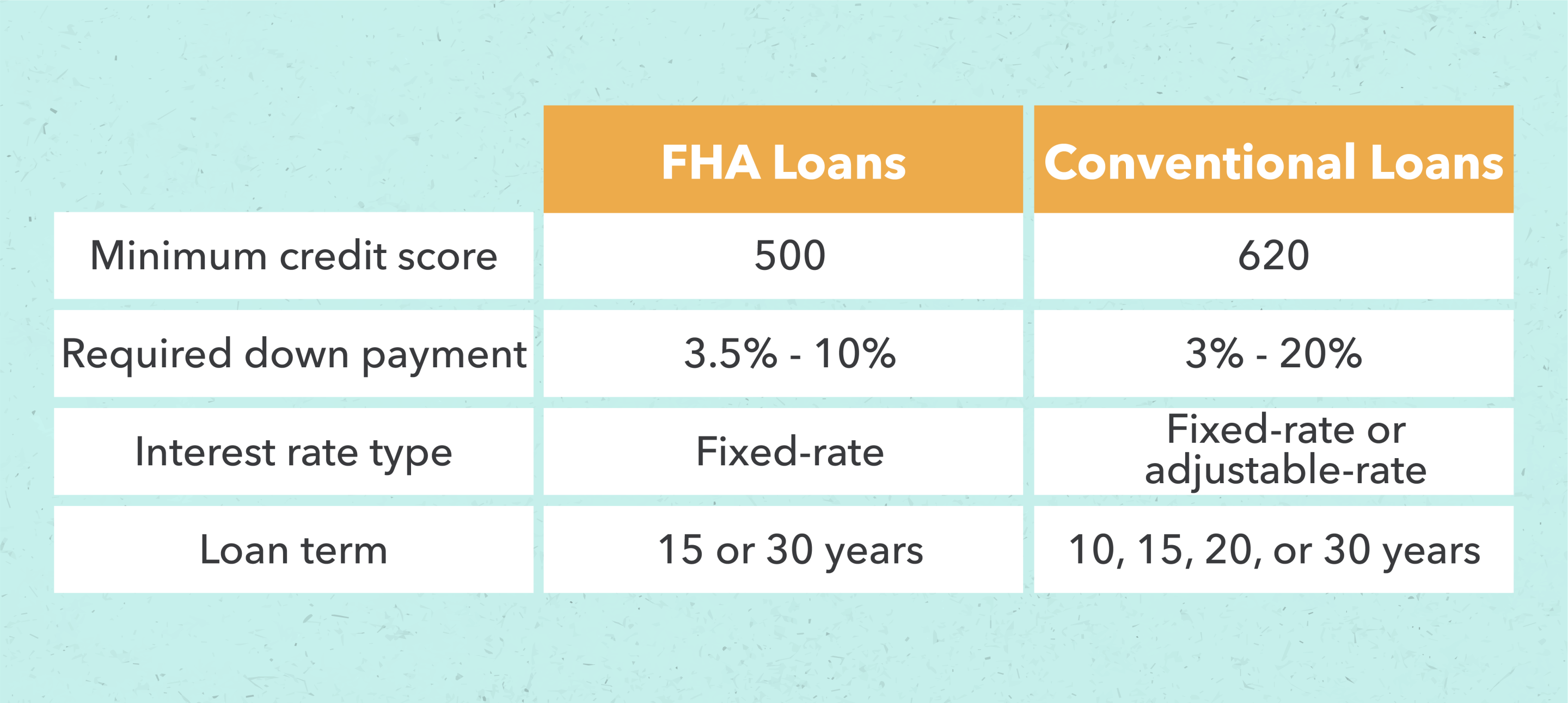

FHA Home Loans vs. Conventional Loans

Understanding the differences between FHA loans and conventional loans is crucial. Your financial planning may vary depending on the type of loan you secure. For example, FHA loans only require a credit score of 500 while conventional loans require a credit score of 620. With FHA loans, you also generally put down a smaller amount—generally 3.5%-10%—while the down payment on a conventional loan can range anywhere from 3%-20%.

Understanding the different loan requirements can help you choose the right loan for your situation. That’s why we’ve provided an FHA home loan vs. conventional loan comparison table below.

FHA Loan Limits

FHA loans come with limits in terms of how much you can borrow to buy a home. Low-cost areas typically have a lower loan limit, while high-cost areas have a higher loan limit. The highest loan limits for FHA loans are in special exception areas.

Keep in mind that FHA loan limits are also dependent on the type of property you’re purchasing. There are different limits for one-unit, two-unit, three-unit, and four-unit properties.

What Are the Pros and Cons of an FHA Loan?

It’s important to evaluate the benefits and disadvantages of an FHA loan to make sure it’s a decision that will help you reach the financial goals you set.

What Are the Pros of an FHA Loan?

FHA loans can be helpful for some home buyers, but it depends on your financial habits, your credit score, and your income. Here are some of the benefits you can enjoy when you secure an FHA loan:

Low credit score requirements. A major benefit of an FHA loan is that it’s one of the easiest loans to qualify for. If you have above a 580 credit score, you’ll benefit from paying a lower down payment, but a low credit score doesn’t necessarily take you out of FHA loan eligibility.

Low down payment. Your down payment is dependent on your credit score, which can be as low as 3.5% if your credit score is above 580. If you have a credit score below 580, you’ll pay 10%, which is still lower than the typical 20% from private lenders.

Assumable mortgage. What many people don’t know is that an FHA loan is also an assumable mortgage, which is the type of loan where the buyer could take over the seller’s mortgage rather than applying for a new loan. This is beneficial to the borrower because even if you have a low credit score, you could still qualify for an FHA loan.

Debt-to-income ratio. What is debt-to-income ratio? This is the percentage that shows how much a person’s income is used to cover his or her debts. The minimum debt-to-income ratios required for FHA loans are 31% for housing-related debt and 43% for total debt.

Borrowing for home repairs. The FHA has a loan for borrowers who want to repair their home called the 203(k) loan. The 203(k) allows you to buy a house and address the necessary repairs in one transaction, or refinance the rehabilitation of your existing home.

What Are the Cons of an FHA Loan?

There are several reasons that might lead you to consider applying for an FHA loan, but these loans are not always right for you. Here’s a breakdown of some of the downsides of FHA loans—especially for borrowers who can qualify for a traditional mortgage:

Low down payment. Although this is most commonly seen as a benefit, a low down payment can also be seen as a drawback. If you only have a low down payment available, it may mean that you’re not quite ready to purchase a home until you start saving money.

Mortgage insurance. There are two types of mortgage insurance premiums to pay — the upfront premium and the annual premium. You typically pay 1.75% for the upfront premium, but the more you borrow, the more you will pay. For the annual insurance premium, you typically pay between 0.80% and 1.05% of your loan balance.

Lender restrictions. The lender must be FHA-approved to offer an FHA loan, but that also means that they can set their own standards for who they approve for the loan.

Minimum property standards. If you’re looking to flip a house, it will need to be in liveable condition to use an FHA loan to purchase it. This is to protect the lender, so if you were to stop making payments on the home, they would be able to resell it.

Loan limits. The FHA changes the maximum and minimum loan amount that it will insure based on the area of the U.S. you live. You can use the FHA Mortgage Limit tool to check the loan limit in your area.

Who Should Consider an FHA Loan?

As mentioned before, first-time home buyers are the most popular candidates for an FHA loan given the requirements to qualify. FHA loans also work well for those who are working on building their credit, don’t have a large down payment, or those who have high debt.

If you’re considering an FHA loan, look at advantages and disadvantages, and compare lenders before making the final decision.

How to Apply for an FHA Loan

The good news is that applying for an FHA loan is fairly straightforward. Here’s how you can apply for an FHA loan today:

Find an FHA-approved lender: Start by finding an FHA-approved lender—these are the only lenders who can offer FHA loans. You can find a list of FHA-approved lenders on the U.S. Department of Housing and Development website.

Gather required documents: Once you’ve found an FHA-approved lender, you’ll need to have valid identification, two years of pay stubs, W-2s or tax returns, and more. Take a moment to gather all the documents you need.

Submit a loan application: Now that you have everything prepared, fill out your application and submit it along with any requested documents. This is the majority of the work when it comes to securing an FHA loan.

Compare loan estimates: Compare loan estimates from different lenders to make sure you’re getting a good rate. Once you’re satisfied with your loan, you can lock it in.

Final Notes

Buying your first home can be an overwhelming experience, especially if you’re trying to decide between FHA loans and traditional mortgage loans. The good news is that Mint can help you budget to buy your first home and prepare for paying your mortgage. With tools like our inflation calculator and the Mint app, Mint makes it easy to keep an eye on your finances. If you need help on your home buying journey, give Mint a try today.

Learn more about home loans:

Discover whether an FHA loan or conventional loan is right for you

Explore the potential benefits of an FHA streamline refinance.

Learn how to get your finances in order to buy your first home.

Learn more about what to look for when you’re house hunting.