Banks make money on the services they provide. They earn money by charging customers interest on various loans and through bank fees.

As hubs for money and financial services, banks deal with lending money and keeping it secured for their customers, but how do banks make money? Much like any other profit-driven business, banks charge money for the services and financial products they provide. The two main offerings banks profit from are interest on loans and fees associated with their services.

Read on for a breakdown of these main services and find out exactly how banks make money from them. Along the way, learn about good money management practices that will prevent banks from making money off of you.

Interest

Interest is what is charged to borrow money. Banks offer customers a service by lending money, and interest is how they profit off of that service. Typically, interest is charged as a percentage of the amount borrowed.

Banks charge interest on a variety of products and services like credit cards, loans, and mortgages. Interest rates vary for different offerings, so take a look at the table below for examples. They also fluctuate over time and based on the economy. For the better part of 2020, 30-year fixed-rate mortgage rates fell to historic lows, hovering around or below 3 percent.

|

Services Banks Charge Interest On |

Average |

|

30-Year Fixed Rate Mortgage |

3.11% |

|

15-Year Fixed Rate Mortgage |

2.61% |

|

Personal Loan |

9.65% |

|

Car Loan |

2.49–6.76% depending on your credit score |

|

Credit Cards |

13–27% depending on card and credit score |

Sources: Freddie Mac 1 2 | Federal Reserve | U.S. News 1 2 |

Whenever a consumer takes out a loan or borrows credit, they’re charged interest until that money is returned to the lender. Let’s use a $5,000 personal loan with the average interest rate of 9.65 percent as an example. If you take two years to pay off the $5,000 personal loan with a monthly payment of $230, you’ll end up paying about $5,566 in total for your loan.

That means that the bank earns $566 in interest from your loan. Banks use a small part of this money earned to pay interest to customers who deposited money in savings or checking accounts. Whatever sum is leftover, the banks keep.

Bank Fees

Banks make a significant amount of their money by charging customers fees to use their financial products and services. Fees take many forms, but they’re often charged to create and maintain a bank account or to execute a transaction. They can be recurring or one-time charges. All banks should be upfront about all of their fees and disclose them somewhere accessible to their customers. Look for a fee schedule online or in the fine print your financial documents.

It’s important to educate yourself on the types of fees that banks impose so that you can be an involved advocate for your own financial wellbeing. Knowing what certain fees are and why they’re charged is a great way to manage the money you keep in the bank and prevent mistakes or errors from eating into your budget. Learn about common bank fees below.

Non-sufficient Funds (NSF) Fees

Non-sufficient funds fees are charged when a customer makes a transaction but doesn’t have enough money to pay for it. The transaction “returns” or “bounces,” and the bank charges the customer an NSF fee.

Overdraft Fees

An overdraft occurs when your bank balance falls below zero. An overdraft fee is charged, and interest can even accrue on the overdrawn amount because the bank may consider that money borrowed as a short-term loan.

ATM Fees

Fees are charged for a few reasons when it comes to ATMs. If you use an ATM that isn’t associated with your bank’s network, you’ll most likely be charged a fee for that transaction. Another fee can be charged if you make too many withdrawals from your account through ATMs.

Late Payment Fees

Fees are charged on credit card or bank statements if a customer misses a payment or pays their bill late. Statements have due dates listed on them whether they’re on paper or online, so make sure you’re aware of these dates in order to not miss a payment.

Minimum Balance Fees

Certain bank accounts have a minimum balance that’s required to remain in the account. If you fall below this minimum balance at any point, you’ll be charged a fee at the end of the month. If you don’t maintain the minimum balance required for your account, your bank may even close your account.

Withdrawal Fees

Depending on your account, you may have a specific number of withdrawals you’re allowed to make per month. Checking accounts are intended for transactional purposes and may allow a certain number of withdrawals before charging a fee. Savings accounts, on the other hand, often put a stricter limit on withdrawals, with the federal limit at six withdrawals. If you make more than the number of allowed withdrawals, you’ll pay a fee each time.

Wire Transfer Fees

A wire transfer fee is incurred when you transfer funds electronically. They’re typically used to transfer money safely and securely across large geographic distances.

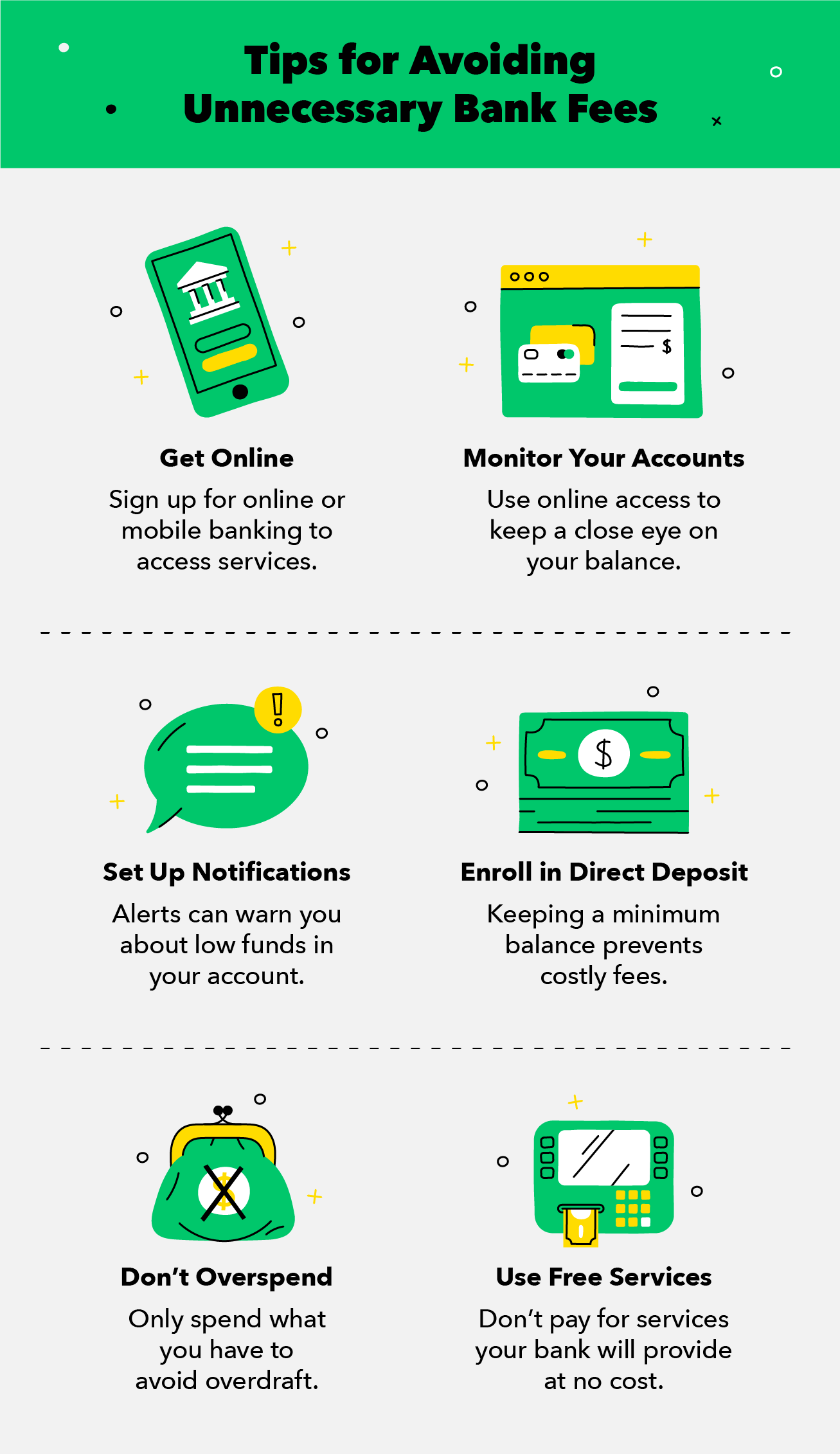

How To Avoid Bank Fees

Banks profit off of charging their customers fees, but there are steps you can take to avoid them. While not all bank fees are avoidable, use these tips to prevent losing money over unnecessary charges.

Tip #1: Take Advantage of Online Services

Most banks have online banking services that allow you to access your accounts remotely. Take advantage of these services by signing up for an online account or logging into your bank’s mobile app. Be careful to not share your login details with others and set up appropriate security measures, like using a strong password or enabling security questions.

Tip #2: Monitor Your Account Balances

Once you have access to an online banking platform or app, use it to keep a close eye on your accounts. Check your account balance so that you don’t overdraw funds and get charged a non-sufficient funds or overdraft fee. Also, use this easy online access to monitor your account for any transaction errors or fraudulent activity. If something does look suspicious, notify your bank immediately.

Tip #3: Set up Automatic Notifications and Payments

Human error can result in costly bank fees. You can use your app or online bank platform to automate loan payments, get notified when a direct deposit is made to your account, and set alerts for when your balance dips below a specific amount or falls into overdraft. Let these processes do the work for you and never spend another cent on bank fees again.

Tip #4: Enroll in Direct Deposit

Direct deposit is another simple automated process that helps you avoid unnecessary fees or consequences. Some bank accounts have a minimum balance in order for them to stay open, and the bank may charge a fee if your account falls below this amount. Set up direct deposit to make sure that your hard earned money gets into your account and keeps it open with no fees.

Tip #5: Don’t Overspend

A good way to never get charged overdraft or NSF fees is to not overspend. Try to live within your means and don’t spend more money than you actually have. Build up an emergency fund so that you won’t need to overdraw your account or take out a loan if the unexpected happens. Balanced money management and preparation are the key to preserving your financial wellbeing.

Tip #6: Try to Use Free Services

Many banks offer free services such as free checking and savings accounts, money transfers, and certain free ATMs. Make yourself aware of these services and their restrictions in order to make the most of them. Try to use ATMs from your bank to avoid ATM fees and pick out a free checking and savings account that fits your needs.

Banks make money off of the interest and fees they charge their customers. Keep your money in your pockets and not the banks’ by following good money management practices. Try to pay off your credit card in full every month to minimize interest payments and monitor your account balances closely so you don’t get charged extra fees. When you practice good money habits, you’ll actively safeguard your financial wellbeing.

Sources: Consumer Financial Protection Bureau 1 2 |