A sinking fund is a sum of money set aside each month that is saved purposefully for a big purchase. Unlike a savings account or emergency fund, a sinking fund offers encouragement to spend it all once you’ve reached your goal.

Saving for a big purchase takes dedication, intention, and strategic planning to reach your goal. One way to intentionally save, and save smart, is by establishing a sinking fund in your budget.

Uses for a Sinking Fund

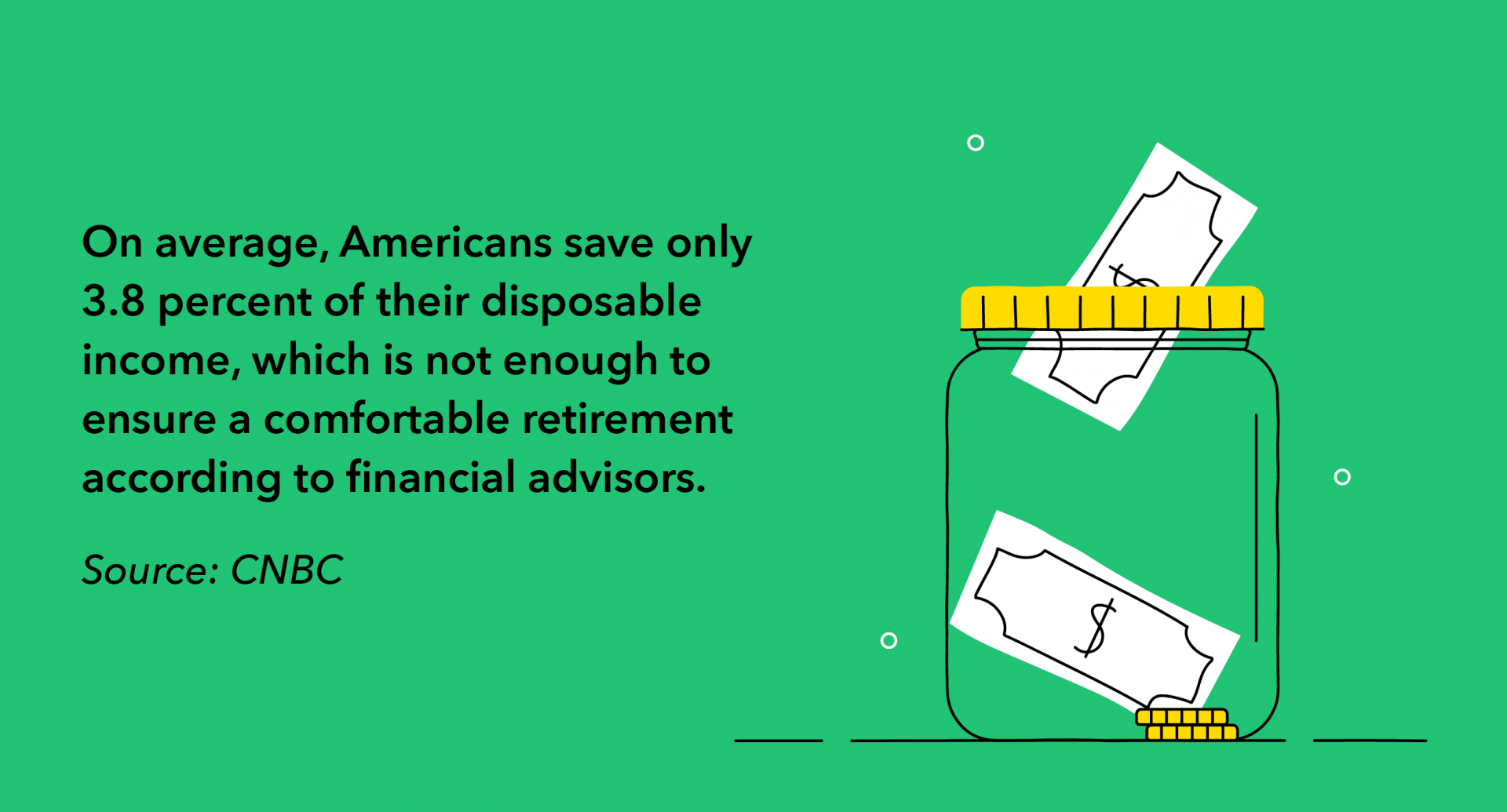

Considering the average American saves less than 5 percent of their disposable income, setting up a sinking fund is a great option for many. It alleviates the need for draining your savings or emergency fund unnecessarily, and is a great solution for keeping you out of debt and on track to meet your financial goals. The best uses for a sinking fund are planned or annual expenses that you can plan for in advance.

Planned Expenses

Some examples of planned, annual, or recurring expenses that would make sense to have a sinking fund for are:

- Large debt: student loans, car payments, significant credit card debt

- Education: tuition, college savings, school fees, school supplies

- Insurance payments

- Dues and memberships

- Gifts: birthday, Christmas, graduation, weddings

- Medical: dentist, vision, primary care physician, emergency room visits

Large Purchases

Another smart use for your sinking fund is saving up for large purchases. Some examples of those large purchases would be:

- Family vacation

- Attending or participating in a wedding

- Buying a car

- Home renovations

How to Create a Sinking Fund

Once you’ve decided to take the leap and set up a sinking fund, setting one up to begin saving is easy. Saving for multiple purchases (meaning multiple sinking funds) is entirely possible, you’ll just have to factor in saving for each of those individual purchases.

Start by figuring out just how much you should be saving to reach your goal, then take the necessary steps to start saving and come closer to making that purchase.

Sinking Fund Formula

The first step to take toward being able to spend your sinking fund is to figure out how much you should save to meet your goal.

First, decide how much should be allocated for the fund, then divide by the number of months you have until you expect the expense or expect to make the purchase. Add those amounts to your budget, while being mindful that you have enough money to cover your regular expenses.

If your sinking fund is being used for something like medical expenses, or anything where you’re unsure of the actual cost, you’ll have to determine a baseline of how much you would like in the account. Set aside the money until you reach that amount, and replenish as needed once you use your sinking fund for its intended purpose.

Set it Aside

The easiest way to set up a sinking fund is to set up an entirely different bank account specifically for your fund. Keeping this account separate from your other checking and savings accounts is important so you know exactly how much is in your fund. This way, you can check regularly and see how much you have saved and how much is left to go.

If possible, set up the money you allotted each month for your sinking fund to automatically be added to your account. Much like saving money, using the “out of sight, out of mind” philosophy when contributing to a sinking fund will make saving not only easier, but you won’t even notice (or miss) the money being added to it.

Once you’ve figured out how much to save and have set up a separate account with automatic transfers, you’re all set to start saving!

Best Accounts for Sinking Funds

The best place to store a sinking fund is in a fairly liquid and easily accessed bank account; such as a high-interest money market account. Each sinking fund is different, and the exact type of account depends on what the fund will be used for, as well as when the money will be accessed.

Saving for a Long-Term vs. Short-Term Goal

If you’re working toward a large goal that is months or even years into the future, like college tuition or a fund for buying a house, you’ll want to opt for a higher-yield account that is less accessible. For goals like this, it’s important to choose a high-interest account. Once you withdraw your funds for your expense or purchase, you’ll be glad you waited a little longer and were able to save more.

It’s important to note that you should not invest your sinking fund in the stock market. No matter how far away you’re planning on making the purchase, you want the funds to be accessible— and grow, not be lost in a crash or poor decision.

For different sinking funds, it may be wise to choose to save in different accounts based on what the fund is intended for. Expenses like emergency room visits or other medical emergencies can pop up at any time, so if you have a sinking fund intended for medical uses you’ll want that money to be stored in a very liquid account to be accessible whenever you need it.

If you’re also planning on putting a down payment on a vacation home, you’ll want to choose a less liquid account since you know when your payment will be due.

Sinking Funds vs. Savings

While a savings account and a sinking fund both have the end goal of money saved, there are key differences between these two accounts.

With a savings account, you are working to build wealth—eventually, you want your savings to work for you, not the other way around. You don’t want to dip into this account, as you want to save as much as you can (and even invest, if your savings doubles as an investment account).

With a sinking fund, you’re saving for a specific purpose. You don’t want to treat your savings and sinking funds interchangeably, as you always want a cushion for anything that may come up.

Sinking Funds vs. Emergency Account

You might be wondering what the difference is between a sinking account and an emergency fund. Though they have the same purpose of a set amount of money set aside, that’s where the similarities end.

An emergency fund should be used for just that—emergencies! Your car breaking down, roof leaking, or sudden job loss are all valid reasons to draw from your emergency fund. You shouldn’t be pulling money from your emergency fund for non-emergencies, because when a real emergency strikes you’ll be relieved you set aside that extra cash for that exact purpose.

A sinking fund is money saved for an exact purpose, that can be spent without guilt or worry that you’re spending what you shouldn’t.

Are You Ready for a Sinking Fund?

The decision to set up a sinking fund can be based on a variety of factors, but the ultimate choice depends on what’s best for you and your personal financial habits.

If you have any big expenses coming up, want to start saving for an extravagant vacation, or are caught unexpectedly when the time for holiday gifts rolls around, starting a sinking fund might be a good idea for you. No matter if you struggle with budgeting for your monthly expenses or follow your budget to a T, it’s always a good idea to have money saved.

Sources: The Fiscal Femme | CNBC | The Balance