If you’re starting to think about paying for college, chances are you’re considering your student loan options. With the average annual cost of tuition, room and board, and other expenses at four-year schools exceeding $40,000 in some cases, it comes as no surprise that 70 percent of students take out loans to pay for college.

Whether you’re thinking about taking out federal loans or private loans, there are many different types. In the world of federal student loans, you’ll likely hear the terms subsidized and unsubsidized loans tossed around a lot. You should understand the major differences between these two types of loans to get a better picture of how much money you’ll ultimately have to pay back in the long run.

What’s the Biggest Difference Between Subsidized and Unsubsidized Loans?

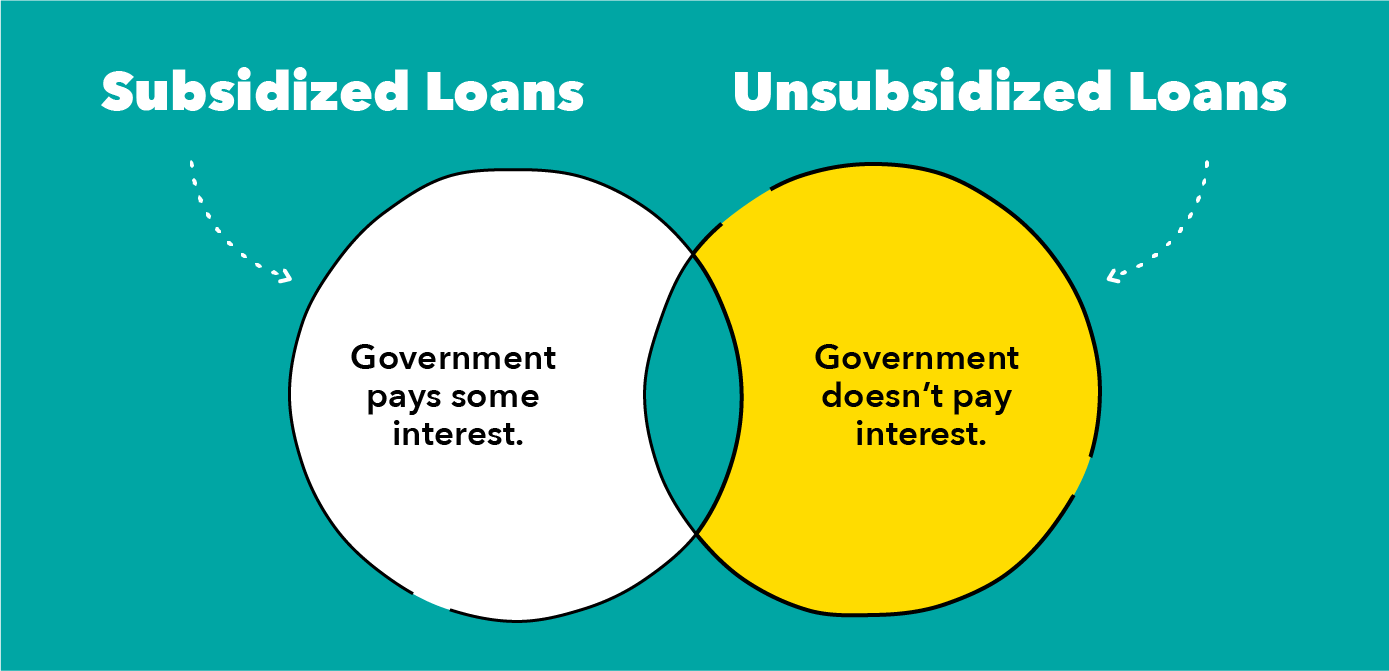

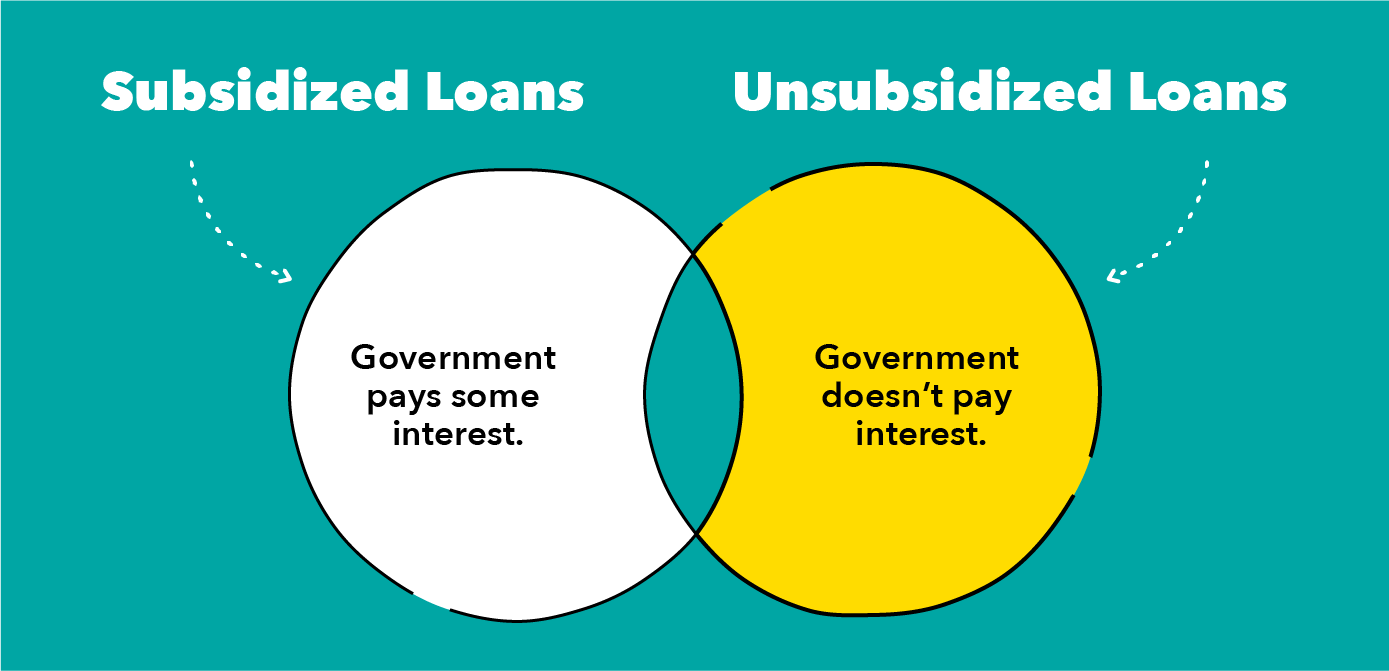

The biggest difference between Direct Subsidized Loans and Direct Unsubsidized Loans, which are both offered by the U.S. Department of Education, is that the federal government pays some of your interest on subsidized loans but does not with unsubsidized loans. Also, subsidized loans are only available to students with financial need.

With a subsidized loan, the Education Department pays the interest on the loan while you’re in school at least half-time (six or more credit hours per term), for six months after you leave school (the “grace period”), and during periods of deferment. Some common examples of deferment include graduate school, unemployment, and active duty military service.

With an unsubsidized loan, you’re responsible for paying all of the interest that accrues. You can choose not to pay the interest while you’re in school and during grace and deferment periods. However, the interest will accumulate during these times and be added to the principal amount when you start paying down the interest again.

If you think that subsidized loans sound like a better deal, you’re probably right. You’ll likely pay less interest in the long term with subsidized loans than with unsubsidized loans. But it’s important to keep in mind that only certain students qualify for subsidized loans.

How Do I Qualify for Subsidized and Unsubsidized Loans?

Your financial need and your education level will be taken into account before you’re offered a subsidized or unsubsidized loan. To receive a subsidized loan, you must be an undergraduate student with a demonstrated financial need. To receive an unsubsidized loan, you can be pursuing your undergraduate, graduate, or professional degree and do not have to demonstrate financial need.

With both loans, you must be enrolled at least half-time at an institution that participates in the Direct Loan Program and be enrolled in a program that will lead to a degree or certificate.

| Direct Subsidized Loans | Direct Unsubsidized Loans | |

|---|---|---|

| Who Pays the Interest? | Education Department while you’re in school, for 6 months after you leave school, and during deferment periods | You |

| Who Can Borrow? | Undergraduate students | Undergraduate, graduate, and professional degree students |

| Do You Need to Demonstrate Financial Need? | Yes | No |

How Do I Apply for Subsidized and Unsubsidized Loans?

Unlike many private loans, these federal loans don’t require a check of your income or credit score. As long as you meet the basic requirements outlined above, you should be good to go.

You must apply for subsidized and unsubsidized loans through the Free Application for Federal Student Aid (FAFSA) form. Your school will typically offer you these loans in your financial aid package, if you qualify. Before receiving any loans, you will need to complete entrance counseling to help you understand the details of your loan and sign a master promissory note agreeing to the loan’s terms.

How Much Can I Borrow with Subsidized and Unsubsidized Loans?

Your school decides which type of loan you can receive each year and the amount you are allowed to borrow.

There are federal limits on how much you can borrow each year. These limits vary based on whether you’re a dependent or independent student and what year you are in school.

In general, you’re a dependent student if you rely on your parents for financial assistance. You will have to report your financial information and your parents’ financial information on the FAFSA. On the other hand, you’re an independent student if the opposite is true. You’ll have to report your financial information and your spouse’s financial information (if applicable) on the FAFSA.

Annual Loan Limits

| Year | Most Dependent Students | Independent Students |

|---|---|---|

| First-Year Undergraduates | $5,500 (no more than $3,500 in subsidized loans) | $9,500 (no more than $3,500 in subsidized loans) |

| Second-Year Undergraduates | $6,500 (no more than $4,500 in subsidized loans) | $10,500 (no more than $4,500 in subsidized loans) |

| Third-Year and Beyond Undergraduates | $7,500 (no more than $5,500 in subsidized loans) | $12,500 (no more than $5,500 in subsidized loans) |

| Graduate or Professional Students | Not applicable (considered independent) | $20,500 (unsubsidized only) |

There are also federal limits on how much you can borrow in total over the course of your studies. For most dependent students, the limit is $31,000 with no more than $23,000 of that coming from subsidized loans.

For independent students who are undergraduates, the limit is $57,500, with a limit of $23,000 in subsidized loans. Graduate and professional students have a limit of $138,500, with no more than $65,500 in subsidized loans.

If you reach the aggregate loan limit over the course of your studies, you can’t borrow any more unless you repay some of your loans. Some graduate and professional students who are enrolled in health profession programs are also eligible to borrow more than the limit in the form of unsubsidized loans.

For How Long Can I Receive These Loans?

You can receive subsidized loans for up to 150 percent of the length of your degree program. For example, if you’re in a four-year program working toward your bachelor’s degree, you can receive subsidized loans for up to six years. (150 percent of four years is six years.)

There’s no time limit on unsubsidized loans.

What are Typical Interest Rates and Fees?

Interest rates vary based on your loan type and whether you’re an undergraduate, graduate, or professional student.

The interest rate on subsidized loans and unsubsidized loans for undergraduate students has hovered around 5 percent for the past few years. The interest rate on unsubsidized loans for graduate students has traditionally been higher, breaking the 6 percent mark. Check the Education Department for current interest rates.

Additionally, there is a loan fee on all subsidized and unsubsidized loans. Currently, the fee is around 1 percent of the loan amount and is deducted from each loan disbursement.

Why Would I Accept an Unsubsidized Loan?

Subsidized loans are usually more preferable than unsubsidized loans because the government helps to cover some of the interest payments. Remember, however, that there are limits on who can take out subsidized loans. You must be an undergraduate student, and you must demonstrate financial need.

If you do not qualify for subsidized loans, unsubsidized loans could be your next best option. Federal loans often carry lower interest rates than private loans and do not require a co-signer if you have no credit history.

Also remember that even though the interest accrues on unsubsidized loans from the time of disbursement, you don’t have to pay the interest on these loans while you’re in school.

Should I Pay Back Subsidized or Unsubsidized Loans First?

Generally, you should pay back unsubsidized loans before you pay back subsidized loans because interest accrues on unsubsidized loans from the time of disbursement and is added to the principal amount.

The interest on unsubsidized loans likely will have grown substantially by the time you start making payments. Since subsidized loans do not accrue interest while you’re in school or during grace or deferment periods, they should have no interest when you begin repayment.

There is some gray area if you have a mix of subsidized and unsubsidized loans with different interest rates. When faced with the decision to pay back a subsidized loan with a high interest rate or an unsubsidized loan with a substantially lower interest rate first, you should probably pay back the subsidized loan first since the unsubsidized loan likely will not have accrued too much interest.

What Are My Repayment Options?

When it comes time to repay your federal loans, there are several options, including: a standard plan that allows you to make fixed payments over 10 years; a graduated plan that allows you to make lower payments at first and then increase your payments over time; or a plan that calculates your monthly payments based on your income. Talk to a financial advisor to assess your options.

You also have the opportunity to apply for a deferment or forbearance that pauses or reduces your payments. If you are enrolling in graduate school or a rehabilitation program, joining the Peace Corps or active duty military service, or are unemployed, you may qualify for deferment or forbearance.

Finally, in some cases, your loans can be forgiven. For example, if you go into public service, such as working at a nonprofit or teaching, you can qualify for loan forgiveness within 10 years, or after 120 payments.

All federal loans are not created the same. It’s important to know the differences between subsidized and unsubsidized loans to know which is right for you and to establish a budget to cover your interest payments down the line.

Sources

StudentAid.Gov | Wall Street Journal | Money Under 30 | Edvisors