You’ve found your dream home and you’re ready to take the next step toward making it yours. After preparing and saving for your big purchase, it’s time to learn how to make an offer on a house. Offer letters are sales contracts and are legally binding, so it’s important to take this process seriously.

Find out everything you need to know about making an offer on a house with this guide. Below is a quick overview of the offer process. Feel free to click on each one to jump to everything you need to know about that step.

Steps for Making an Offer on a House:

- Determine you can afford the house and decide to make an offer.

- Talk with your real estate agent about comparable homes before making an offer.

- Your real estate agent compiles a written offer.

- The written offer is sent to the seller’s agent.

- The seller replies and your offer is accepted, countered, or declined.

- Learn how to compete with multiple buyers.

- The closing process begins when your offer is accepted.

- Remember to negotiate before finalizing if contingencies reveal flaws with the house or deal.

- Once your offer is accepted, you finalize the contract.

What to Know Before Making an Offer on a House

In addition to researching the process of making an offer, learn these key tips to keep in mind throughout.

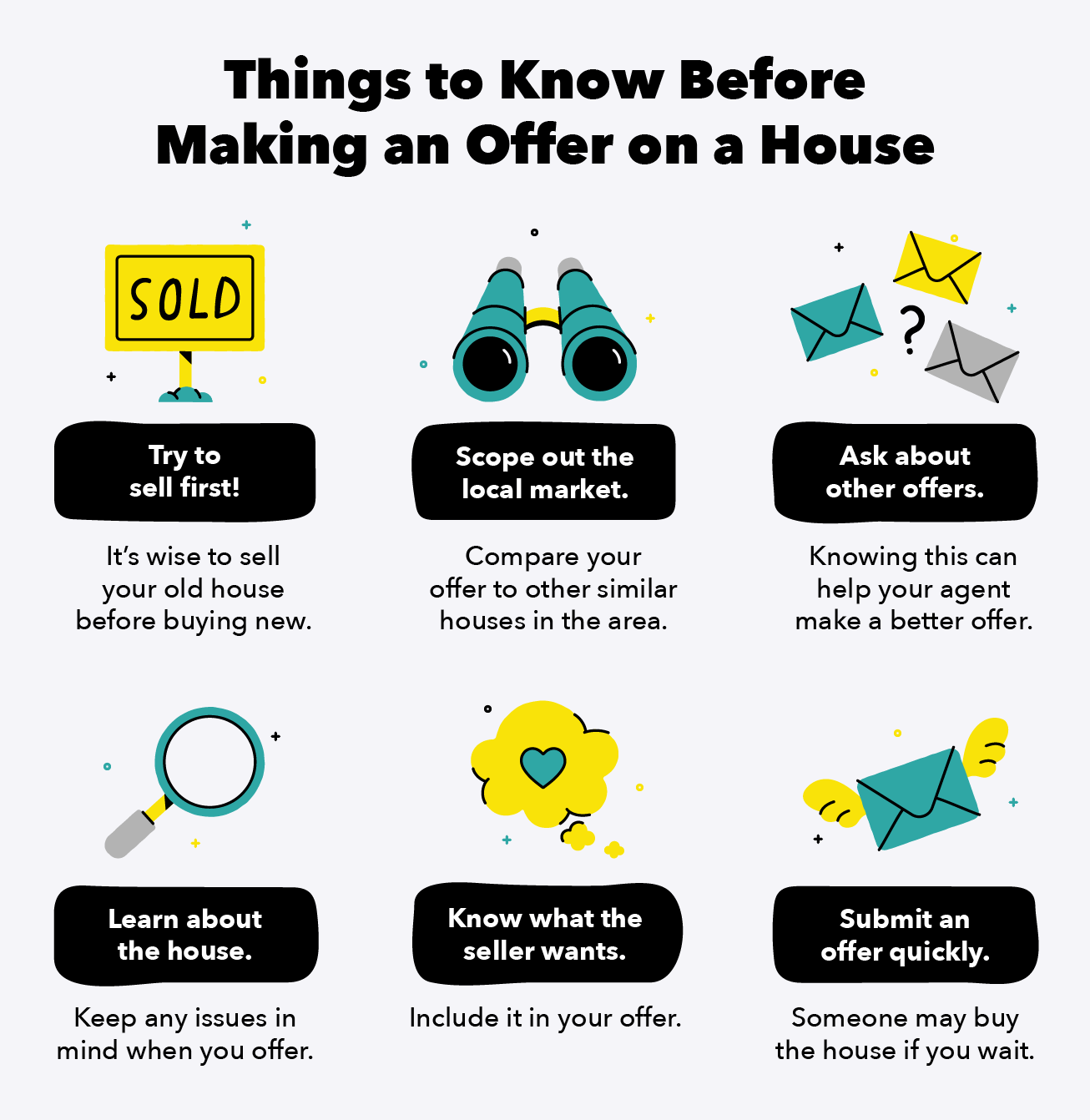

- Try to sell first and buy after. If you aren’t a first-time homebuyer, it’s a good idea to sell your current home before buying a new one. This is important if you’re using the sale of the old home to purchase the new one.

- Scope out the local market. Your real estate agent will use information on similar houses for sale in the area to put together your offer.

- Ask about other offers. Your agent does this for you. Sometimes the seller’s agent won’t disclose this, but this information can inform your offer.

- Learn about the house. If there are problems with the house, you’ll want to find out and keep them in mind when you make an offer.

- Know what the seller wants. Have your agent find out what appeals to the seller and try to include it in your offer. If the house still has a mortgage, offering an early payment can help tip the balance in your favor.

- Act fast. For the best chance at your dream home, submit an offer quickly. Don’t wait around because someone else will likely snap it up if you hesitate.

Step 1: Determine Affordability of the House

Finding your dream house is the easy part. Figuring out if you can afford it takes a hard look at the numbers. Set a home budget beforehand and be strict about sticking to it when looking at houses. To gauge what your budget should be, a majority of lenders advise that you shouldn’t spend more than 28 percent of your monthly pre-tax income. Be sure to include your estimated monthly payment plus other costs like the down payment, HOA fees, home insurance, and property taxes in your budget.

When you go through the lending process, lenders can help you determine what is affordable. If you’re not there yet, use this home affordability calculator to see if your dream house is in your budget.

Step 2: Talk with Your Real Estate Agent

Making an informed offer is the key to giving you the best chance of getting the house you want. Speak with your real estate agent about what comparable homes in the area are going for and use this information to guide your offer.

Step 3. Compile an Offer Letter

After comparing similar houses for sale, you’ll work with your agent on your offer. There are many components to an offer letter. We discuss everything that is included, how to navigate your offer price and contingencies, and tips for making an offer they can’t refuse.

What’s Inside an Offer Letter

Offer letters are legally binding sales contracts, and it’s important to be thorough about what you include.

Typical Components of an Offer Letter:

- Offer price: This is the amount of money you are willing to pay for the house.

- Contingencies: Conditions that the seller must abide by if and when they accept your offer. Standard contingencies include a home inspection and appraisal. Jump down to learn more about contingencies.

- Down payment: The amount paid for the home upfront. This can be anywhere between 3 to 20 percent when paired with a conventional loan.

- Earnest money: This is a deposit made by the buyer to demonstrate good faith on a contract to buy a home. It’s generally a small percentage of the price and is held in escrow until the offer is closed. It’s usually applied to the down payment or closing costs once the offer is accepted.

- Closing costs: These include all costs associated with purchasing a home. Read more on some of the common closing costs like inspection and loan origination fees.

- Timeline: You’ll include your preferred closing date, as well as the closing date of your current home if you aren’t a first-time buyer.

How Much Should You Offer?

Figuring out how much you should offer depends on what you can afford and what kind of market you’re dealing with at the time of the purchase. Your real estate agent should guide you through making an offer, but ultimately, you are the one who decides what you’re willing to pay. A good rule of thumb is that your first offer should leave some room for negotiation, so don’t give away what you’re willing to pay right away.

Making an Offer in a Buyer’s Market

In a buyer’s market, you have more power to negotiate because there is more supply than demand. With the bargaining advantage on your side, you can feel more comfortable making an offer below the asking price. If you do offer below asking price, negotiation is a typical response.

When offering less, it’s also important to be respectful of the seller. Offending them with an outrageously low offer could result in them rejecting and you losing your dream house.

Making an Offer in a Seller’s Market

A seller’s market is when the housing demand exceeds the supply. In this situation, you will not have the bargaining advantage, and you will be competing with others for attractive properties. If you can afford it, exceeding the seller’s asking price can help you stand out among other offers. Remember to keep your budget in mind when negotiating and don’t offer an amount you can’t afford.

Contingencies

Contingencies are conditions of the purchase that get outlined in your offer and must be met for the sale to go through. If they aren’t met, based on the contingency, either the buyer or seller can cancel the sale. About 74 percent of buyers include contingencies in their offers, so let’s discuss the standard ones below.

Home Inspection Contingency

A home inspection contingency exercises your right to have the property inspected before closing the sale. If the inspection reveals problems with the house like faulty plumbing or a compromised structure, there is room to remedy any issues before you close. You can negotiate for a lower price, ask the seller to make repairs, or even back out of the offer.

It’s not advisable to forego a home inspection contingency to make your offer more attractive. This could cause you to pay more for a damaged property and could cause financial problems down the line if you find out there are major issues with the house that are costly to fix. Home inspections prior to closing are always recommended.

Home Appraisal Contingency

A home appraisal contingency verifies that the price you are paying is fair compared to the home’s market value. In the event that the house you are buying is appraised as lower than the selling price, you are able to negotiate with the seller or cancel the contract. This is recommended to prevent you from paying more than you should for a house.

Home Sale Contingency

In case you need to sell your current home in order to finance a new one, you can make a home sale contingency. This contingency stipulates that the current house must be sold before the new purchase can close.

Home sale contingencies aren’t attractive for sellers, as they cause delays and discourage other offers. A clause can be attached to this contingency by sellers to include a sell-by date. If your house hasn’t sold by the date in the clause, the seller is legally able to move on with other offers.

Financing/Mortgage Contingency

A financing or mortgage contingency allows the buyer time to secure financing from a lender. For buyers, this provides insurance that they can cancel the sale and recover their earnest money in case their financing options fall through.

This contingency is usually given a specific timeline, and the buyer can end the contract before time expires. If the buyer has not secured a mortgage and fails to cancel the contract before the allotted time is up, they will still be obligated to purchase the property.

Tips For Making an Offer They Can’t Refuse

When making an offer on a house, remember to appeal to the seller by using these tips to make an offer they can’t refuse.

- Make an offer in cash. If you have the savings and can afford to make an offer in cash, you can forego the financing contingency. This means less delay in the sale, and it can also help you compete with higher offers with more contingencies.

- Propose a short closing period. If you’re willing to move quickly, offering a short closing period can appeal to a seller who needs to sell fast.

- Pay some of their closing costs. All sellers will have closing costs when the sale goes through. Paying off some of those costs can help sweeten the deal for them.

- Offer up more earnest money. More earnest money shows you’re serious about the home. It’s also more money in the seller’s pocket upfront.

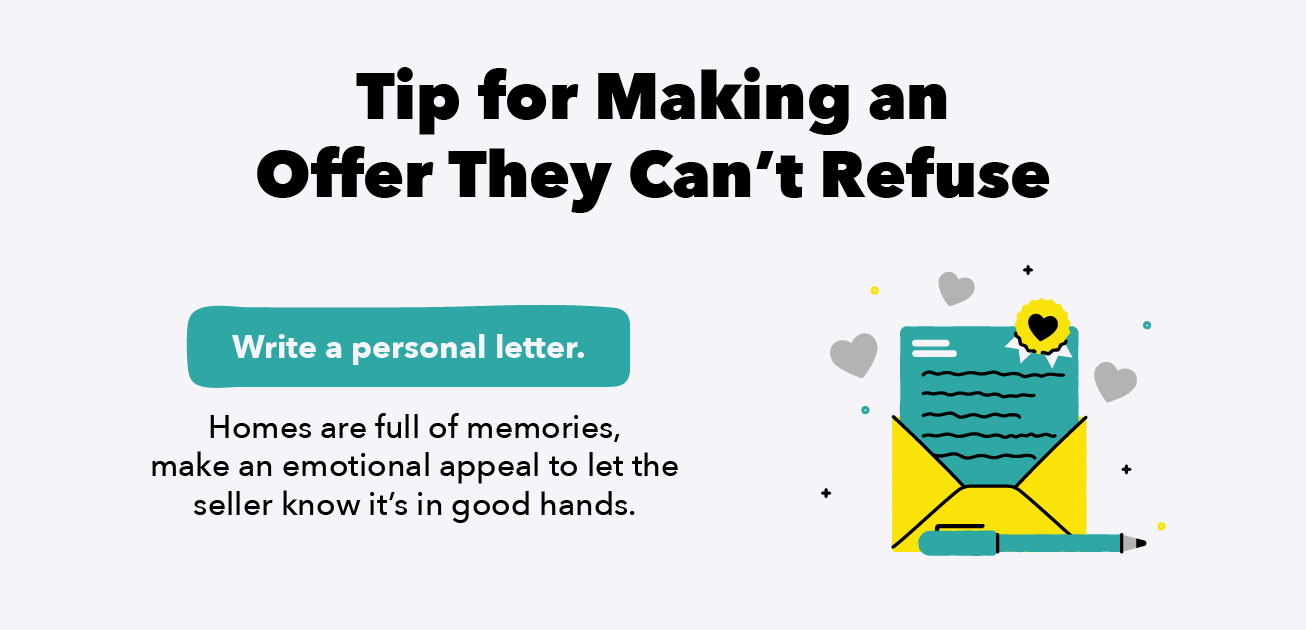

- Write a personal letter. Homes are very personal and sellers may be emotionally attached to them. Make an emotional appeal by writing a personal letter to tell them the home will be in good hands.

Step 4. Submit Your Offer

Once you have decided on an offer, your real estate agent will write up a purchase and sale agreement. You will sign this agreement and then they will submit it to the seller’s agent. This agreement is legally binding if the seller agrees.

Step 5. Review Seller’s Reply

A seller can reply in a couple of ways. They can accept, counter or decline. Let’s walk through what to do with any of these three responses and what to do when there’s another buyer.

What to Do When They Accept

Congratulations — they’ve accepted your offer! You can now move on to Step 7 of the offer process. As long as all contingencies are met, you are buying a house.

What to Do When They Counter

The seller might not have liked your offer exactly how it was written and they can counter. It’s then up to you to accept that offer or to start negotiating by countering again. You are also free to back out of the offer if you aren’t happy with the seller’s counteroffer.

If you do end up negotiating, it’s normal for there to be a back and forth of counteroffers. You are both working to come to an agreement on price, timeline, and contingencies, and this takes time.

What to Do When They Decline

Unfortunately, if the seller declines, you won’t be buying that particular house for what you offered. If there is room in your budget, you could attempt to make a more attractive offer. About 45 percent of buyers end up making multiple offers during the buying process. However, not every budget allows for a better offer.

A declined offer is a disappointing outcome, but it’s important to be respectful of the seller’s decision. Take the time to talk to your real estate agent and learn about what can be done differently when the next opportunity comes around.

Step 6: How to Compete With Multiple Buyers

In a competitive housing market, desirable properties will attract many buyers. Here are a few potential scenarios that can play out if a seller receives multiple offers.

Multiple Buyer Scenarios:

- If your offer didn’t compare with the others, they may decline you and pursue other offers.

- If your offer was one of the better offers, they may ask each buyer to return with their best offer and make a decision among those final offers.

- They may allow a bidding war to see who will come up with the best offer.

Strategies for Competing With Multiple Offers:

- Be flexible with your contingencies. Keep important ones like the home inspection and appraisal, but figure out which ones aren’t necessary for you.

- If there is room in your budget, add an escalation clause. This notifies the seller that you will outbid the highest offer up to a maximum amount. This shows you are serious and keeps you competitive price-wise.

- Mention preapproval for a mortgage if you have it. The more likely you are to obtain financing, the more attractive you are as a candidate.

- If you can afford it, increase your down payment or earnest money deposit.

To keep everything professional, remember that your real estate agent should facilitate negotiations directly with the seller’s agent.

Step 7: Start the Closing Process

The closing process begins when a buyer accepts your offer. This process includes all necessary actions that must be done to move the transaction forward like reviewing what you owe, authorizing documents, and transferring the title. For an in depth walkthrough of this process, check out this guide for closing on a house.

Step 8. Negotiating After Your Offer is Accepted

When a seller accepts your offer, you will first move forward with any contingencies. If anything is wrong with the house or deal, you have the ability to negotiate or even walk away. Here are some examples of negotiations based on contingencies:

- If a home inspection reveals flaws with the house, you can ask for repairs to be made by the seller before the deal is closed so that the financial burden doesn’t fall to you.

- If the home is appraised to be lower in value than the accepted offer price, negotiate for a lower, more appropriate sale price.

Step 9: Finalize Your Contract

When negotiations have ended and you are satisfied with your contract, you will sign to finalize your purchase. Once you sign, the contract is legally binding.

After you make it through the final step, it’s time to celebrate! Revel in the excitement of purchasing your dream home, and know that you just took a big step toward a new life. Keep up good saving and budgeting habits so you can continue to hit your financial goals in the future.

Sources: Investopedia