Save more, spend smarter, and make your money go further

After learning the basics of saving money in previous chapters of our savings series, you may be eager to know exactly where you can keep your funds safe.

Since 94.6% of U.S. households have a checking or savings account, you may already have one of these types of accounts. But it’s important to understand the full scope of the differences between savings vs. checking accounts so you can use them to their full potential. Having the right checking and savings account is important for making the most of your money.

In Chapter 4, we’ll guide you through the intricacies of maintaining a checking or a savings account to protect and grow your funds. Keep reading or use the links below for a detailed comparison of checking vs. savings accounts.

Checking Account: What is It & What’s the Primary Purpose?

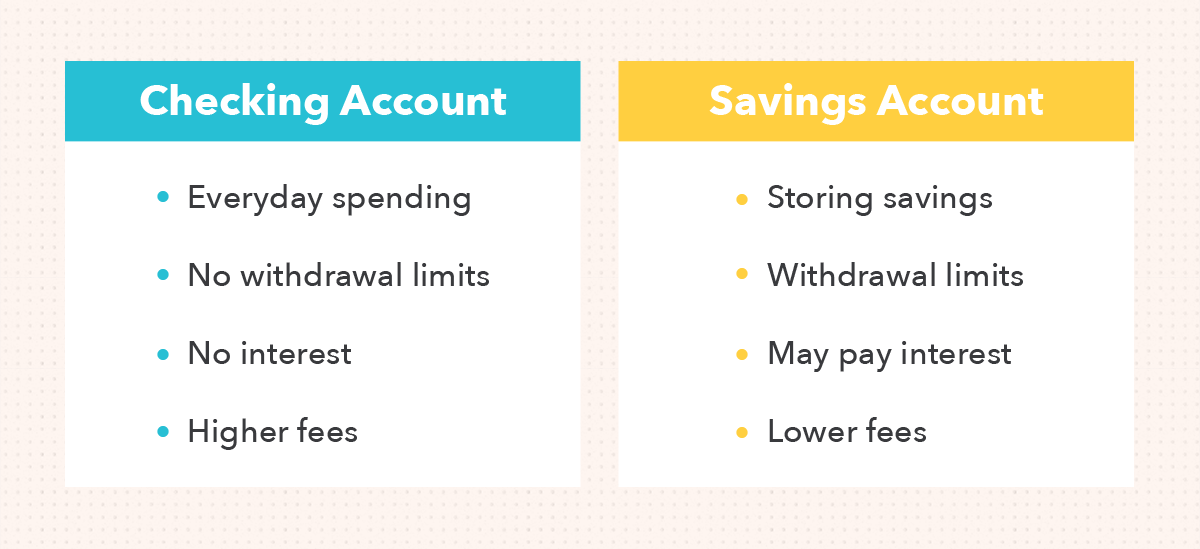

A checking account allows you to make an unlimited number of deposits and withdrawals through various avenues. This makes it ideal to be used as a regular account, which lets you transfer funds, make payments, and use the ATM whenever you want. Checking accounts were originally named as such because they allowed you to write paper checks.

When you are making a comparison between a checking account vs. savings account, you may also notice that checking accounts are mainly favored for making everyday transactions. This is because a checking account is designed to help you store and spend your money. This also makes it the account you use to manage your living expenses.

To make it easy to use your checking account, financial institutions provide you with various ways to use and access your checking account. This includes debit cards, checkbooks, and online banking apps for seamless money transfer. Your credit card will be separate, even if it’s with the same bank and allows you to make payments by transferring money from your checking account.

How Do Checking Accounts Work?

With their primary purpose of helping you make your daily transactions, checking accounts are used for the majority of your banking needs. Whether you want to receive funds from a family member or pay utility bills through a banking app, these accounts are typically used.

Checking accounts have many attributes, with the most popular including the following distinctions.

- They are built for making daily transactions.

- They are managed and protected by a variety of banks and credit unions.

- They can be operated individually or with a partner in the form of a joint account.

- They typically don’t provide you with any profit against your deposit.

- They have little-to-no service charges for maintaining your account.

- They offer different types of financial instruments including debit cards and checkbooks.

You can open a checking account through a variety of avenues such as a popular bank or credit union. But you may want to open your account with a bank that offers Federal Deposit Insurance Corporation (FDIC) insured accounts or a federally insured credit union that is covered through the National Credit Union Share Insurance Fund.

It’s because these insured accounts cover your deposits for up to $250,000 per depositor, which means that it can cover up to $500,00 for joint accounts. This means that if the bank or credit union fails, you should be able to retrieve your funds for up to the defined limit.

Why Do You Need One?

A checking account is an essential part of banking that gives you access to a variety of features, benefits, and services. Through a checking account, you can manage your professional and personal financial needs.

Having a checking account allows you to:

- Store your funds at a secure location.

- Deposit funds using cash and checks.

- Withdraw your funds in emergency situations through debit cards and checkbooks.

- Make online payments through your bank account.

- Receive money from others such as your employer, family, and friends.

- Maintain financial records through bank statements.

- Build your budget template based upon your transactions.

- Operate third-party accounts through financial apps.

Due to these important offerings, checking accounts stand out as an imperative financial avenue for everyone to have. Whether you are calculating cost of living for your family or writing checks for donations, your checking account can cater to your financial requirements with ease.

What Are the Advantages

There are several advantages of opening and operating a checking account on an active basis.

Some of the most common benefits include:

- Withdraw your money anytime, anywhere. You can access an expansive network of ATMs to withdraw your funds using a debit card. Through a checkbook and online banking apps, you may also enjoy other avenues of money transfer.

- Get paid without added risks. With a checking account, you can set up direct deposits with your employer and steer clear of the possibility of losing your paychecks or having them processed quickly so you can get your money right away on payday.

- Maintain your funds without excessive charges. A checking account typically won’t have a maintenance fee attached to it. If it does, you might be able to have it waived under the financial institution’s terms and conditions.

- Keep a record of your transactions. Through online and printed bank statements, you can keep a record of your financial transactions. This gives you a full picture view of your deposits and withdrawals and makes it easier to make a financial plan.

- Have peace of mind with intensive security. Banks and credit unions that offer checking accounts often have extensive security in place, including advanced cybersecurity measures. If the institution goes out of business, federally-insured accounts may also recover your funds.

What Are the Disadvantages

There are also disadvantages associated with checking accounts. You need to be mindful of these potential drawbacks so you can choose a checking account that best suits your needs and utilize it the greatest advantage.

The potential downsides of checking accounts include:

- You typically cannot earn any interest. While some checking accounts offer you minimal returns in line with your deposits, most of them don’t offer interest—regardless of how much amount you deposit within them. This means that if you are saving your money in a checking account, you may be missing out on an opportunity to grow your funds.

- You have to be wary of transaction charges. Many checking accounts come without maintenance fees, while others have certain fees attached to them for operating the account. With that being said, these fees can be waived at a variety of financial institutions. This outlines the requirement to look through your options and read the fine print of available offerings. One thing to keep in mind is that you’ll want to learn how to budget carefully so you don’t incur overdraft fees which can add up quickly if you find yourself in a bind.

- You have to think about balance maintenance requirements. Some checking accounts may also require you to maintain a minimum balance. This requirement varies upon the financial institution that you choose for your checking account. Keeping this in mind, you may want to explore different offerings and choose one with little-to-no minimum balance requirement.

Savings Account: What is It & What’s the Primary Purpose?

A savings account allows you to deposit your money with a financial institution, while also giving you a certain level of return on your account balance. Savings accounts typically allow only a limited number of withdrawals through an account routing number. More often than not, they also don’t offer a debit card or checkbook to use to take money out, only the option to transfer funds to your checking account.

This design makes savings accounts an avenue to store your money instead of using it regularly. When making a comparison of savings vs. checking accounts, these profit-bearing and limited transaction mechanisms stand out as some of the most glaring differences between the two.

But this focus on limited transaction services also makes savings accounts so well suited for growing your funds. These accounts also come with different interest rates that help you increase your funds by simply storing them with your choice of financial institution.

Typically, a high yield savings account offers the best returns against your money, but these rates also come with fluctuations due to market movements. You can go back and read Chapter 3 in the series to learn how to choose a savings account that best suits your goals.

How Do Savings Accounts Work?

When you deposit your money into a savings account and let go of unlimited access to your funds, your bank returns the favor by providing you with certain profits or yields against your balance.

This is because when you show an intention of not actively using your savings account funds, your bank can freely invest your money into its lending and investment products. This way, the money you deposit is used to generate profit for the bank.

Many savings accounts calculate your interest on your balance. Often, banks will compound interest annually and add the interest you’ve built up onto your balance once a year.

You can always withdraw the interest you’ve earned, but you can also leave it and allow it to compound further over the course of the next year. This can help you generate the greatest earnings in the long run. To make an informed decision, you can use an investment calculator.

For most basic savings accounts, the interest rate is fairly low, but you can shop around.

Why Do You Need One?

Many individuals who have a checking account for daily transactions still open a savings account with the sole purpose of putting their money away for future use. While some people open a savings account simply to stash away money for future use, you may need a savings account to grow your funds for a specific purpose.

Here are some reasons you may want to open a savings account:

- You intend to practice money-saving habits.

- You want to build an emergency fund over time.

- You plan to save for big purchases such as a home down payment.

- You need to achieve short-term goals such as taking a vacation.

- You require a head start on fulfilling long-term goals such as building a college fund.

- You plan to save for a comfortable or early retirement.

- You want to have enough funds at hand to get into higher investments.

Which type of savings account is best for your specific goals will become more clear when you compare your options side by side.

What Are the Advantages

There are various benefits to opening a savings account. These perks typically focus on helping you grow your funds through the account over time.

The following points outline some of the most common advantages of a savings account:

You earn interest on your account balances. Earning interest on your account balance is the most basic yet biggest benefit of having a savings account in place. Through high-yield savings accounts, you can also find options with higher-than-usual interest rates. This helps you with building savings and growing your funds.

You may find it easier to save money with the restrictions that prevent spending. When you have a savings account, its restrictions on withdrawals as well as the unavailability of debit cards and checks act as additional money-saving steps. In many instances, this may keep you from making instant withdrawals without a second thought. As a result, you are able to lean towards saving instead of spending money.

You can fulfill a variety of financial goals. Saving money is the basis for achieving many of your life and financial goals. If you’ve used our retirement savings calculator and seen how far away from your ideal savings you are, setting up a dedicated account can help. It’s also great for establishing an emergency fund, saving for a down payment, and more. Your savings account can help you work toward a variety of financial objectives.

You may use it as a ladder to higher investments. When you have little-to-no savings on hand, using a savings account can help you learn how to better manage your money and build up some wealth. Besides fulfilling your spending goals, these additional funds can also help you be able to afford to take the next step into higher investments.

You can enjoy peace of mind thanks to security measures. Savings accounts also come with insurance by the FDIC for banks and the National Credit Union Share Insurance Fund for credit unions. In addition to physical security, these insurance elements help you recover your funds for up to $250,000 per depositor in the event of the financial institution going out of business. For joint accounts, this limit goes up to $500,000.

What Are the Disadvantages

Savings accounts also come with a certain set of drawbacks. Once you learn more about them, the process of setting and achieving goals becomes easier for you in the long run.

You have to put up with minimum balance requirements. More often than not, savings accounts come with the requirement of minimum balances. If you don’t cater to these conditions, you have to pay certain charges in return. Or, you might not be able to open an account at all.

It’s harder to withdraw your funds at a moment’s notice. The restricted withdrawal model of savings accounts can act as a double-edged sword when you need to access your funds right away. You’ll have to take a few steps to access those funds so you can use them.

You have to maintain higher balances to earn higher returns. You can start a savings account with a fairly small account balance if you want. But in order to earn notable interest, you may want to consider building up a higher account balance. With that being said, the long-term profit on any balance is better than nothing at all.

Bottom Line: You Shouldn’t Have One Without the Other

While comparing checking vs. savings accounts, you may have realized that for many people it makes sense to have both for the greatest financial stability. This not only allows you to make your regular transactions with ease, but also lets you save your funds with beneficial offerings in the long run.

You may easily open both types of accounts at the same financial institution, while also enjoying the federally-insured account benefits for each of your checking and savings accounts. This provides you with convenience without compromising your financial security. However, you can always shop around for the account that offers the greatest benefits—which might just be the lowest fees in some cases.

This concludes the fourth chapter in our savings series. Next up is Chapter 5: How to Calculate Savings Goal.Sources: Federal Deposit Insurance Corporation (FDIC) 1, 2 | National Credit Union Administration (NCUA)

Save more, spend smarter, and make your money go further