Once you decide to become a homeowner, it’s likely that you will need to take out a mortgage to purchase your new home. While the conclusion that you need a mortgage to finance your home is usually easy to arrive at, deciding which one is right for you can be overwhelming. One of the many decisions a prospective homebuyer must make is choosing between a 15-year versus 30-year mortgage.

From the names alone, it’s hard to tell which one is the better option. Under ideal circumstances, a 15-year mortgage mathematically makes sense as the better option. However, the path to homeownership is often far from ideal (and who are we kidding, under ideal circumstances we’d all have large sums of money to purchase a house in cash). So the better question for homebuyers to ask is which one is best for you?

To help you make the most informed financial decisions, we detail the differences between the 15-year and 30-year mortgage, the pros and cons of each, and options for which one is better based on your financial priorities.

The Difference Between 15-Year Vs. 30-Year Mortgages

The main difference between a 15-year and 30-year mortgage is the amount of time in which you promise to repay your loan, also known as the loan term.

The loan term of a mortgage has the ability to affect other aspects of your mortgage like interest rates and monthly payments. Loan terms come in a variety of lengths such as 10, 15, 20, and 30 years, but we’re discussing the two most common options here.

What Is a 15-Year Mortgage?

A 15-year mortgage is a mortgage that’s meant to be paid in 15 years. This shorter loan term means that amortization, otherwise known as the gradual repayment of your loan, happens more quickly than other loan terms.

What Is a 30-Year Mortgage?

On the other hand, a 30-year mortgage is repaid in 30 years. This longer loan term means that amortization happens more slowly.

Pros and Cons of a 15-Year Mortgage

The shorter loan term of a 15-year mortgage means more money saved over time, but sacrifices affordability with higher monthly payments.

Pros

- Lower interest rates (often by a full percentage point!)

- Less money paid in interest over time

Cons

- Higher monthly payments

- Less affordability and flexibility

Pros and Cons of a 30-Year Mortgage

As the mortgage term chosen by the majority of American homebuyers, the longer 30-year loan term has the advantage of affordable monthly payments, but comes at the cost of more money paid over time in interest.

Pros

- Lower monthly payments

- More affordable and flexible

Cons

- Higher interest rates

- More money paid in interest over time

|

15-Year Mortgage |

30-Year Mortgage |

|

|

Pros |

• Lower interest rates • Less money paid in interest over time |

• Lower monthly payments • More affordable and flexible |

|

Cons |

• Higher monthly payments • Less affordability and flexibility |

• Higher interest rates • More money paid in interest over time |

Which Is Better For You?

Now with what you know about the pros and cons of each loan term, use that knowledge to match your financial priorities with the mortgage that is best for you.

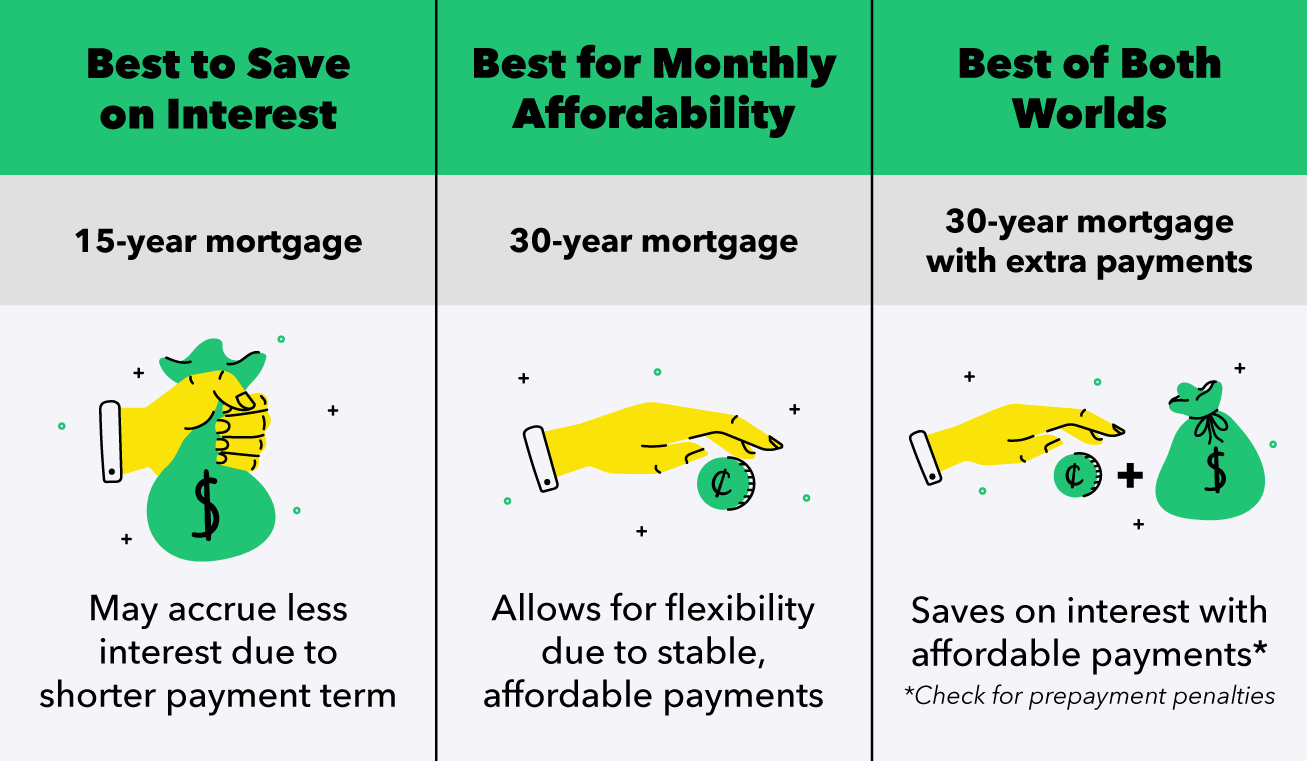

Best to Save Money Over Time: 15-Year Mortgage

The 15-year mortgage may be best for those who wish to spend less on interest, have a generous income, and also have a reliable amount in savings. With a 15-year mortgage, your income would need to be enough to cover higher monthly mortgage payments among other living expenses, and ample savings are important to serve as a buffer in case of emergency.

Best for Monthly Affordability: 30-Year Mortgage

A 30-year mortgage may be best if you’re seeking stable and affordable monthly payments or wish for more flexibility in saving and spending your money over time. The longer loan term may also be the better option if you plan on purchasing property you couldn’t normally afford to repay in just 15 years.

Best of Both: 30-Year Mortgage with Extra Payments

Want the best of both worlds? A good option to save on interest and have affordable monthly payments is to opt for a 30-year mortgage but make extra payments. You can still have the goal of paying off your mortgage in 15 or 20 years time on a 30-year mortgage, but this option can be more forgiving if life happens and you don’t meet that goal. Before going this route, make sure to ask your lender about any prepayment penalties that may make interest savings from early payments obsolete.

As a prospective homebuyer, it’s important that you set yourself up for financial success. Fine-tuning your personal budget and diligently saving and paying off debt help prepare you to take the next steps toward buying a new home. Doing your research and learning about mortgages also helps you make decisions in your best interest.

When picking a mortgage, always keep in mind what is financially realistic for you. If that means forgoing better savings on interest in the name of affordability, then remember that path still leads to homeownership. Try out these budget templates for your home or monthly expenses to help keep you on a good path to achieving your goals.

Sources: Consumer Financial Protection Bureau