Save more, spend smarter, and make your money go further

Income tax is the tax that federal, state, and local governments require businesses and individuals to pay on their total earnings each year. Total earnings can include wages, tips, interest, dividends, unemployment, and retirement distributions.

To calculate income tax, you must first determine your taxable income and filing status to see which tax bracket you fall into and the total deductions you qualify for. Once you calculate how much of your total income for the year is taxable, you can determine the amount of federal and state income taxes you owe.

When you file your IRS Form 1040 at the end of the year, you’ll already have an idea of how much you can expect to pay in income taxes or if you’ll qualify for a refund.

How Income Tax Works

Regardless of your immigration status, if you are working and making an income in the United States, you are required to pay federal income taxes on your total earnings to the Internal Revenue Service (IRS) each year. Based on the guidelines set by the IRS, you’ll calculate your taxable income by factoring in deductions and exemptions. Then, you’ll see if you qualify for any tax credits before determining the total amount you owe in taxes.

The government uses these personal income taxes to fund national security, roads, schools, government services, and programs like Social Security.

Calculating Taxable Income

Taxable income is the amount you earned over the course of the year that is subject to taxes. It’s equal to your gross income, or annual income, minus the deductions and exemptions you qualify for. When filling out your Form 1040 to pay taxes, you’ll calculate your taxable income using the total wages, tips, and other compensation found in box 1 of Form W-2.

Exemptions

Tax exemptions like charitable donations or dependant exemptions reduce your taxable income and the amount you owe in taxes. Since the standard deduction increased with the Tax Cuts and Jobs Act of 2017, personal exemptions for 2022 have been eliminated.

Standard vs. Itemized Deductions

When filing your taxes, you can choose to itemize your deductions or take the standard deduction based on your filing status. You would only want to itemize if your qualified deductions are more than the standard deduction.

If someone can claim you as a dependent, you can take a standard deduction of $1,150, or your total earned income plus $400 — whichever is greater. If this total exceeds the standard deduction for your filing status, then you’ll use the standard deduction listed below instead.

These rates are based on the Revenue Procedure 2021-45 from the IRS.

Understanding Your Federal Income Tax Bracket

Based on your filing status — single, married filing jointly, married filing separately, or head of household — and your taxable income, you’re placed in a federal tax bracket that determines your tax rate and how much tax you owe.

What is Federal Income Tax Withheld?

Federal income tax withheld is the amount removed from your paychecks over the course of the year that goes towards taxes. This number can be found in box 2 of Form W-2, which you’ll receive from your employer at the end of each year.

What Tax Bracket Am I In?

Once you calculate your taxable income, you can look at the current federal tax bracket based on your filing status and determine the taxes you owe. You can find your taxable income on line 37 of Form 1040.

The seven income tax brackets for 2022 range from 10 percent on income less than $10,275 to 37 percent on income equal to $539,900 or more for single filers. Below, you can find the effective tax rate based on your filing status and taxable income.

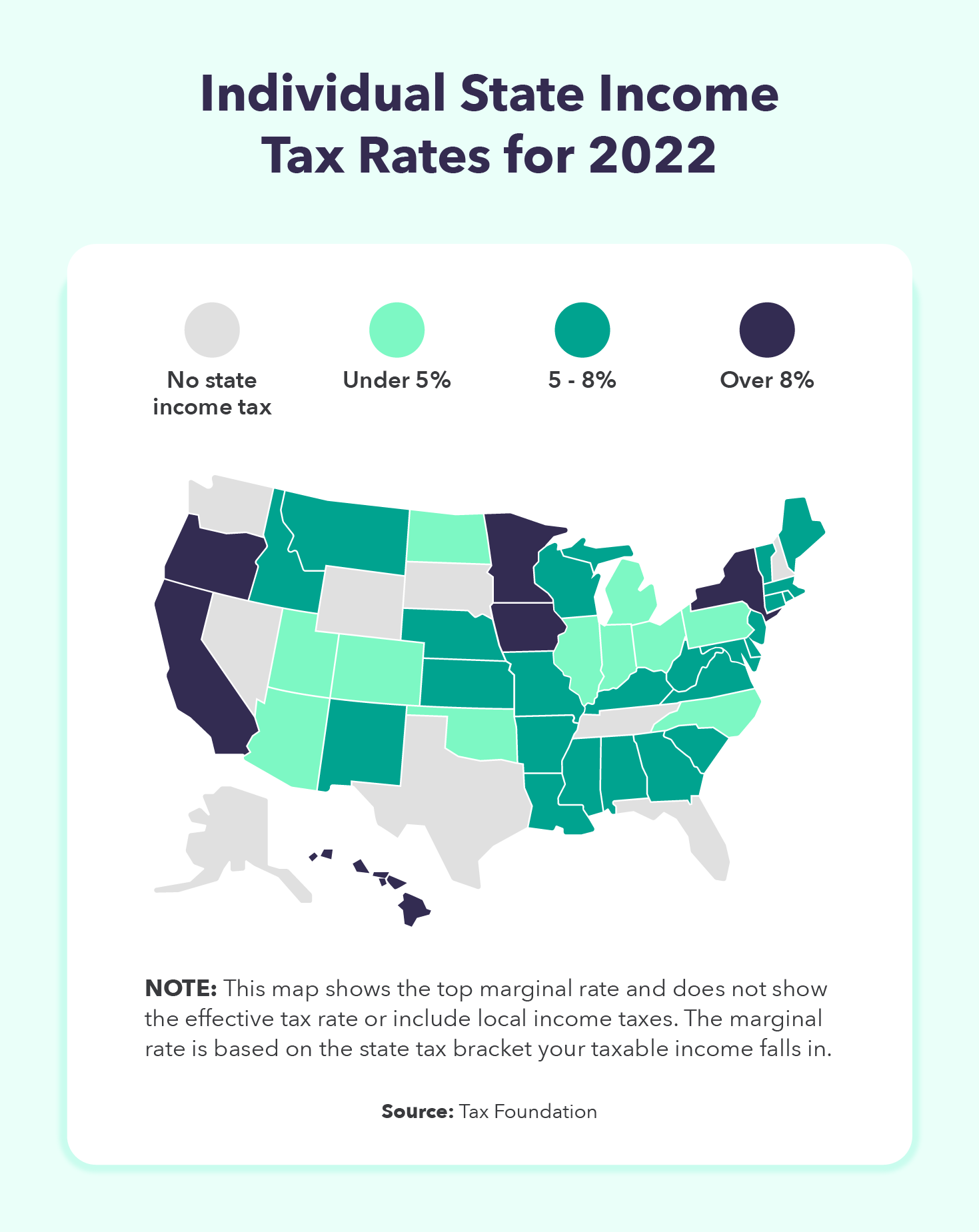

State and Local Income Tax

Only nine states in the U.S. — Texas, Florida, Tennessee, Alaska, Nevada, Washington, New Hampshire, Wyoming, and North Dakota — don’t collect state income taxes. The other 41 states either levy a flat or graduated-rate income tax.

Tax Credits

While deductions reduce your taxable income, tax credits reduce the amount of tax you owe, also known as tax liability. If your tax credits are greater than the amount of taxes you owe, you could be entitled to a refund. Be careful to follow IRS rules for how to calculate your tax credits before claiming them on your tax return.

Individuals can qualify for family and dependent credits, income and savings credits, homeowner credits, health care credits, and education credits. The child tax credit and dependent care credit are some of the most common tax credits individuals qualify for.

How Do I Pay Taxes or Get a Refund?

Once you determine the amount of federal and state income taxes you owe for the year, you have a few options for paying them. If you’ve filed a Form W-2 with your current employer, they will take out a portion of each of your paychecks to go towards your income taxes throughout the year — this is your tax withheld.

Many people end up paying slightly more throughout the year than what they actually owe in income taxes. When filing your return, you’ll calculate how much you actually owe. If you overpaid, you’ll qualify for a tax refund.

If you haven’t had income taxes taken out of your pay throughout the year or you owe more than what was taken out, you’ll need to pay the taxes you owe when you file with the IRS. By calculating your income tax, you can estimate how much you’ll owe in taxes so you can budget throughout the year and follow our tax planning strategies to lower your tax liability and decrease tax season stress.

Our budgeting app makes it easy to set aside money every month to pay your taxes at the end of the year and even track your refund after you file.

Sourcing

Save more, spend smarter, and make your money go further

-

Previous Post

WTFinance: Annuities vs Life Insurance