APR stands for “annual percentage rate.” In terms of credit cards, it is the baseline rate used to calculate how much interest you’ll pay on any balance you carry over into future billing cycles.

Every credit card has an APR but it’s not the same for every person with that card. Your personal rate is determined through your credit score/report. And if you have a good credit score, your APR may be lower than if you had a poor credit score.

How APR Works

The short answer: it depends on how you use your card.

If you pay your balance in full every month, your APR won’t affect you at all because you aren’t borrowing money from a creditor.

But if you carry a balance over to the next billing cycle, you’ll have to pay interest on that balance each day past the date it was due. Your credit card’s APR is how they calculate that interest.

To do so, your credit card company divides your APR by the number of days in a year. This gives them what is known as your “Daily Periodic Rate” or the amount of interest they charge you each day past your balance’s due date.

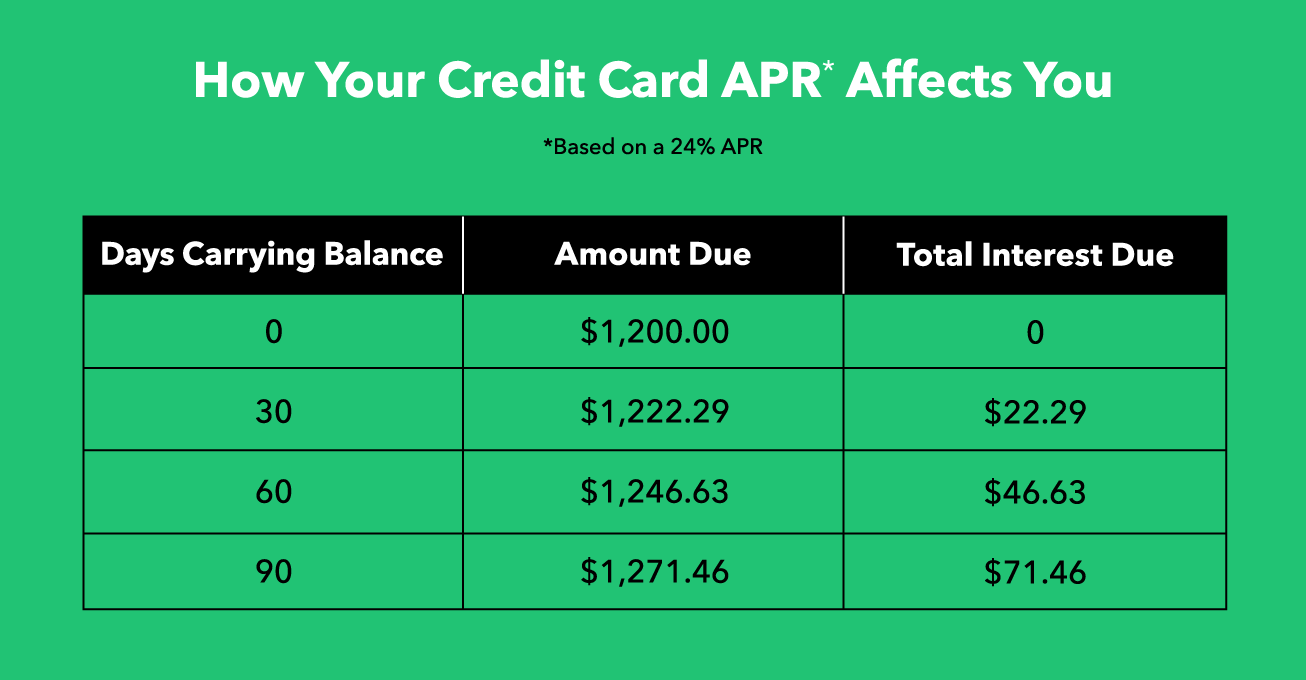

For example, if your APR is 24 percent, you’d pay 0.066 percent (24 percent/365) interest on your current balance each day until you pay it off — including on any interest you were charged from previous days.

So if you waited 15 days into the next billing cycle to pay off a balance of $1200, that means you’d owe an additional $10.30. And if you were to wait until the next billing cycle to pay it off (30 days), you’d owe an additional $22 on top of your original balance.

Here’s what you’d owe after three months, assuming your APR didn’t change (more on that in a second):

It’s important to note that a 24 percent APR is higher than average. Here’s what constitutes a good credit card APR.

What Is a Good APR for a Credit Card?

Most credit card APRs are variable, meaning they fluctuate based on a standard rate set by another organization. In the case of APRs, it’s usually the Prime Rate, which is the interest rate that banks provide their best customers (the Prime Rate fluctuates based on the interest rate set by the Federal Reserve).

That means an excellent APR is the one that is closest to the Prime Rate (which would be the lowest).

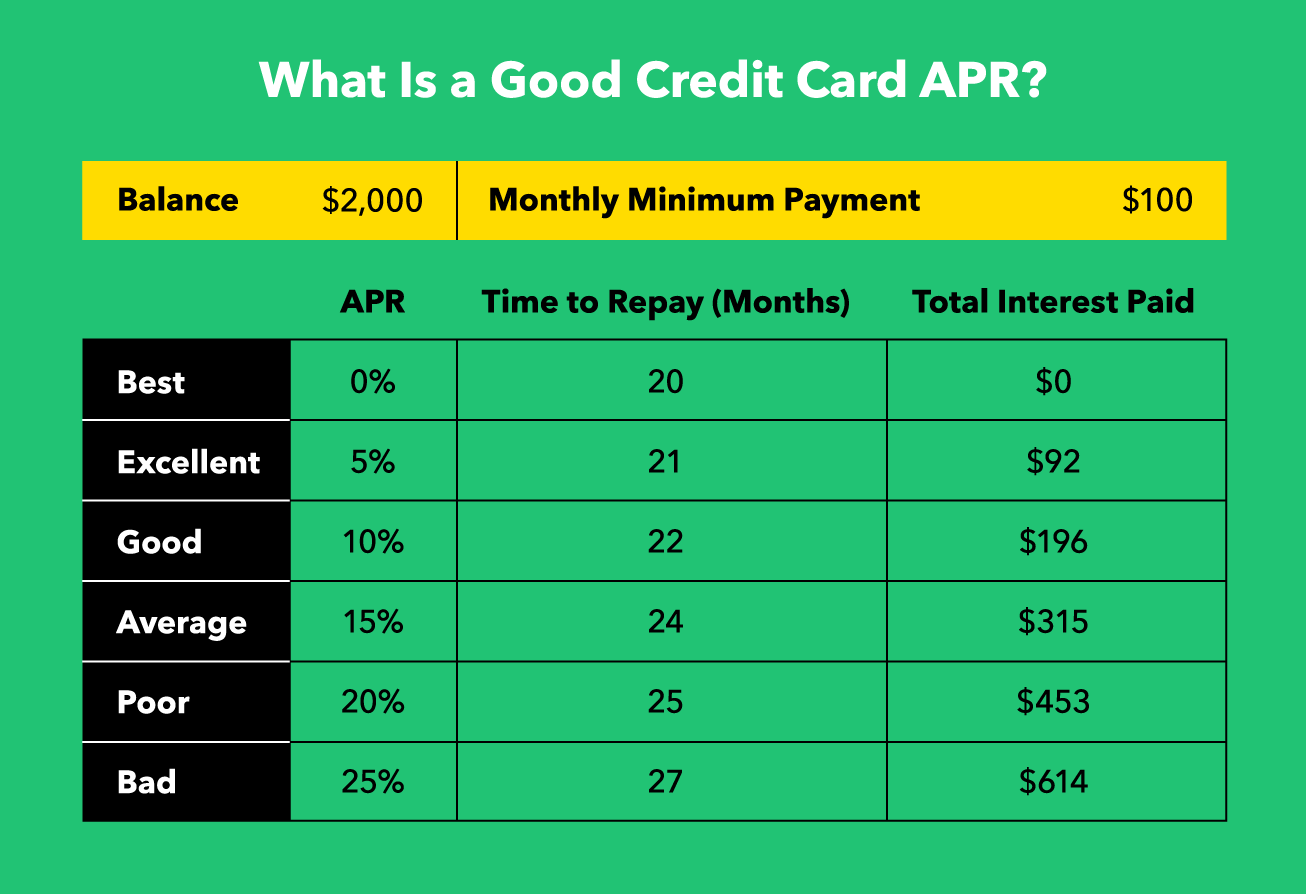

The national average for credit cards is around 15 percent according to the Federal Reserve. So many would consider anything lower than that “good.” Here is a breakdown of how different hypothetical rates would affect you, assuming a constant balance and monthly minimum payment:

The most important takeaway is that a lower APR is always better, especially if you regularly carry a balance. Here are some additional things to be aware of when comparing APRs for different credit cards.

5 Different Kinds of APRs Your Credit Card Typically Has

The APR we’ve discussed so far is what is known as your Purchase APR. This is the APR used to calculate the interest on any purchase you make that you don’t pay off on time.

However, credit cards often have more than one kind of APR associated with them — each of which serves a different purpose.

Introductory APR

Introductory APRs are usually offered as a promotion to get you to sign up for a new card. It will typically be lower than your normal rate (this is where you’ll typically see a zero percent APR) and only lasts for a certain period of time after you first sign up for the card.

Balance Transfer APR

Your Balance Transfer APR is the interest rate that’s applied to any balances you move from one card to another. Sometimes they have a promotional period associated with them like an Introductory APR would.

Cash Advance APR

This is the interest rate that’s applied to any cash you withdraw from an ATM with your credit card. It’s usually higher than your Purchase APR and typically applied to convenience checks as well.

Penalty APR

This is the interest rate that’s applied to any TOS (terms of service) violations. It’s usually the highest of all of your APRs and is also applied when you wait more than 60 days to pay off a balance.

Fixed vs. Variable APRs

Most credit cards have variable purchase APRs. However, some credit card APRs remain fixed, meaning your interest payment will be the same for a given period of time. That said, it doesn’t mean the rate will never change — it just means that your credit card issuer will likely have to contact you before they do.

Fixed APRs are not common and most frequently coincide with promotional/introductory offers.

How to Get the Best APR on a Credit Card

The best APR is the one you don’t use. Not only because it saves you from paying interest, but also because it could help you improve your credit (which, in turn, improves the APR you qualify for).

Here are a few additional tips for lowering the APR you qualify for:

1. Improve Your Credit Score

Since your credit card’s APR is influenced in part by your credit score, the more you can do to improve it, the lower your APR will be. Keep in mind some easy ways to improve your credit score.

2. Make Payments On Time

If you pay your credit card bill on time, you’ll avoid paying interest altogether. But you’ll also reduce the amount you’ll pay if there’s ever a day you need to carry a balance as well.

That’s because your payment history is 35 percent of your credit score. A long track record of paying your bills on time could help you improve it.

Credit card companies also look at this as well to determine what your APR should be.

3. Reduce Your Credit Utilization

It’s a general rule that keeping your credit utilization below 30 percent will help you improve your credit score. However, some studies show that people with the best credit score keep their utilization below 10 percent. Either way, lower is better, so focus on reducing your credit utilization.

A quick and easy way to do that is to increase your credit limit on your existing cards.

4. Monitor Your Credit Report

Sometimes bad credit isn’t your fault. It’s not uncommon for things which adversely impact your credit to appear on your report unbeknownst to you.

That’s why you should regularly check for negative activity that might adversely affect your credit (and APR). The good news is, checking your credit report is easy (and free).

5. Open One Loan or Credit Card at a Time

Although it’s temporary, opening several lines of credit at once can put a big dent in your credit score.

For example, if you take out a mortgage and open a credit card in the same month, or apply for three new credit cards all at once, it could lower your score significantly — especially if you don’t have a long history of on-time payments.

It’s always best to open one line of credit at a time to keep your credit score from dropping too far (and your APR from skyrocketing).

Boosting your credit score so you qualify for a better APR won’t happen overnight, but it is possible to achieve with the right work. Not to mention, the total benefit you’ll see in your financial life is significant. So here are six more ways to improve your credit score.