A mortgage is a loan given by banks (or other financial institutions) to those who plan to purchase a home. There are many types of mortgage loans available, depending on your financial health and how long you want to pay the loan back. The amount you’re allowed to borrow — as well as the interest rate — can vary depending on your credit history and the market.

It’s important to know all the mortgage options you have available, including key terms you’re bound to hear when approaching potential lenders. You’ll be making payments on this home for the next 15 to 30 years, after all, so understanding what you’re signing is crucial to ensure you’re making the best decision for your future.

After you’ve saved enough for a down payment, read up on the next steps in the process to help boost your financial health. Below, we’ve put together a guide on what a mortgage is, including the ins and outs of the type of loans you’ll get to choose from.

Table of Contents:

How Does a Mortgage Work?

Under a mortgage agreement, the bank, credit union, or other lender lets the customer borrow money to purchase a home in exchange for monthly payments with a tacked on interest rate. The “mortgage” itself refers to the lender’s ability to take back the home if the borrower misses payments, also known as a collateral loan. While the buyers technically own the home, the lender has the power to cash in on the collateral of the home if the buyer defaults on payments.

Parties Involved

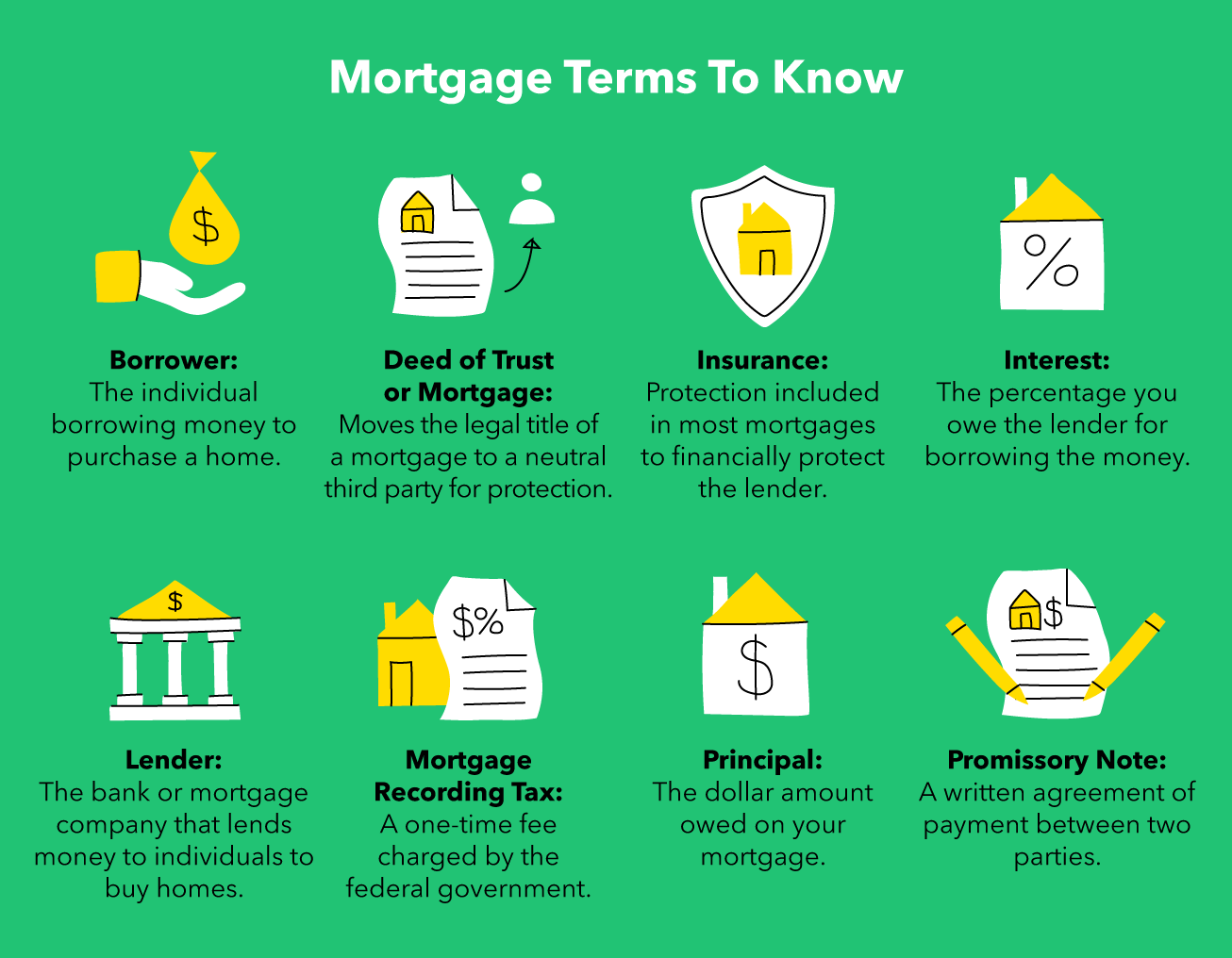

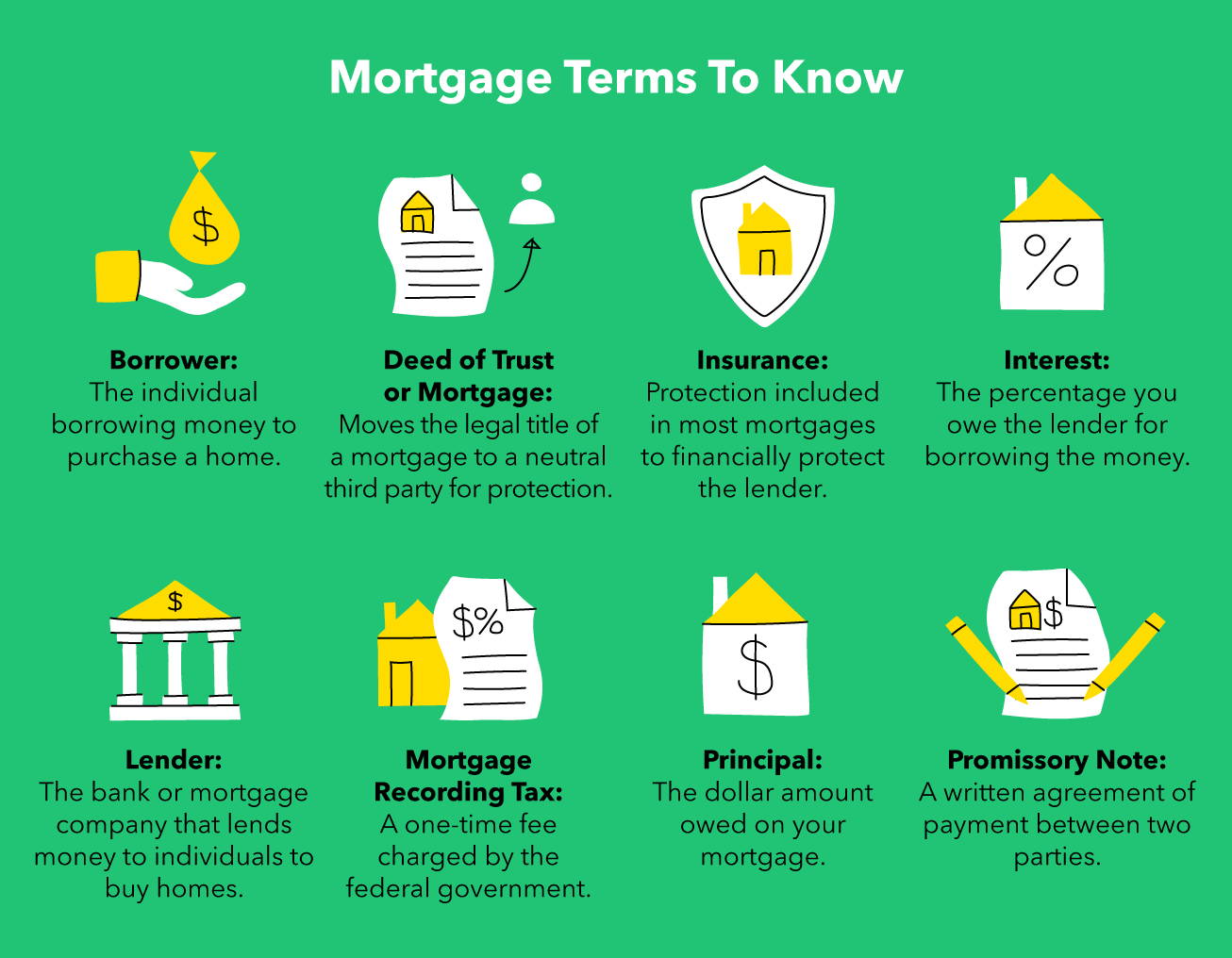

The two main parties involved in a mortgage loan are the lender and the borrower. A lender is a bank or other financial company that lends out money to customers to help them make larger purchases such as a car or home. A borrower refers to the individual(s) that will be borrowing money from the lender and paying it back over a set period of time.

The Main Parts of a Mortgage

There are various factors and real estate terms that get thrown around when discussing a mortgage. Some of the most important sections within a mortgage loan are the principal, interest, insurance, the length of the loan and taxes. Below, we break down the unique terms you might come across as well as the mortgage loan basics.

Principal

The principal is the dollar amount owed on your mortgage, usually noted in both the total amount as well as monthly payments on your loan. For example, if the house is for sale for $230,000, and you put down 20 percent ($46,000), you would need to take out a loan for the remaining principal amount of $184,000.

Interest Rate

The interest rate is the percentage that you owe the lender for borrowing the money, on top of the original principal amount. Mortgage interest rates currently average around 4 percent, but can reach as low as 2 percent on shorter loans or for borrowers with a good credit score and robust credit history. You’ll often see interest rates marked on loans as APR (annual percentage rate) which adds in other borrowing costs outside of the principal interest. As this rate is required on all loans, you can compare APR’s on multiple mortgage offers to make sure you are taking advantage of the best deal.

You can help get this interest rate lowered by taking advantage of mortgage points. This process allows you to make upfront payments to your lender for a reduced interest rate that spans the life of your mortgage loan. To get one mortgage point, you have to pay 1 percent of your total mortgage up front. And while costly, these points can help save you money over the length of your loan by lowering your monthly interest rate.

Insurance (PMI)

Typically, there is a portion of the loan agreement that discusses mortgage loan or private mortgage insurance, as the lender will want to be financially protected in case you aren’t able to make your payments. This is more common for borrowers with low credit scores or those who weren’t able to put down at least 20 percent of the cost upfront.

Taxes

In some states, there are taxes you need to be aware of when moving forward with a mortgage loan. Property taxes are set by your local government (and sometimes your state government as well), and are grouped along with your hazard insurance and can be escrowed.

A mortgage recording tax is a one-time fee charged in all 50 states. You can expect to see additional charges (on top of the recording tax) during closing in the following states: Alabama, Florida, Kansas, Minnesota, New York, Oklahoma, and Tennessee.

Promissory Note

A promissory note is a written agreement of payment between two parties. It’s the legal document that you sign when getting a mortgage loan, and it includes how much you will pay the lender each month and for how long. It also documents the next steps if the borrower isn’t able to pay, which is also known as defaulting on a loan.

Mortgage Amortization

Mortgage amortization is the process of splitting up the principal and interest amounts owed into equal payments over the length of your loan. While the amount of money that goes towards your interest and principal varies over the length of your loan, this process ensures that your overall monthly payment is the same. For example, at the beginning of your loan, most of your monthly payments will go towards interest. However, over time you will owe less interest and the majority of your monthly payment will go towards the principal.

Escrow

Traditionally, escrow refers to the securing of the transaction when buying a home. The buyer transfers money to an escrow company while the homeowner does the same with their property. By taking each asset to a reliable third party, the transaction is secured while final inspections are made.

When getting a mortgage from a lender, an escrow account refers to the amount of money your lender takes from your monthly payments to pay for home insurance and other taxes on your behalf (this payment is not always required). In addition to taking money each month, most lenders will require upfront payment to cover several months (sometimes as many as six months) before they will move forward with the mortgage loan.

Types of Mortgages

There are a few options to consider when looking at the type and length of mortgage loan to move forward with. There are 15 and 30-year mortgages as well and fixed and adjustable interest rates to consider. Below, we break down the types of mortgages to help you make the best decision before signing a loan.

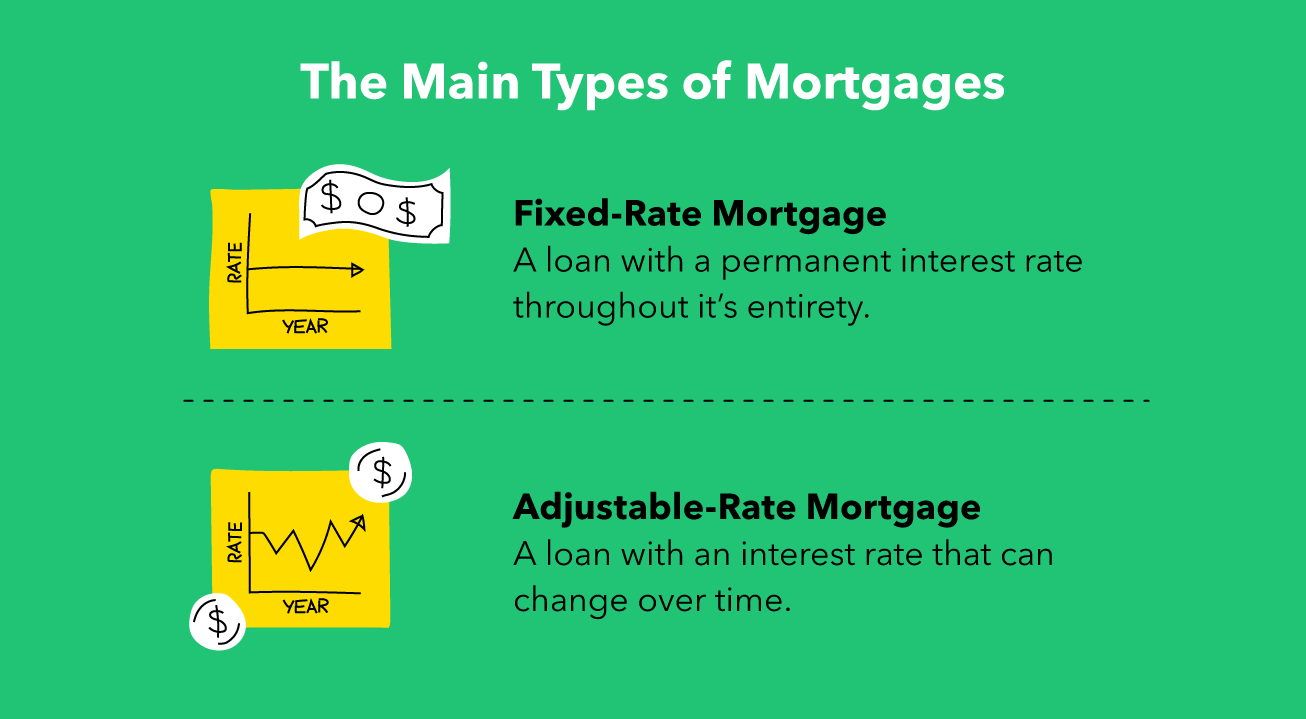

Fixed-Rate Mortgage

A fixed-rate mortgage is a mortgage loan whose interest rate is permanent throughout the entirety of the loan (no matter if it’s a 10- or 30-year loan). While fixed-rate mortgages mean there won’t be a spike in interest if market rates increase, it also means that borrowers must refinance to take advantage of lower rates. Fixed rate mortgages are the least risky of all loans and a 30-year fixed mortgage is the most popular loan type used.

Adjustable-Rate Mortgage

Adjustable-rate mortgages (ARM), also called floating or variable rate mortgages, have interest rates that will fluctuate according to an index (such as the LIBOR) lenders and their margin rate. Typically, these rates will change yearly from the time of signing. Often, ARMs have annual and lifetime caps, meaning the change can’t be too drastic from year to year.

ARMs are structured with an initial rate set for a predetermined amount of time, ranging from one to ten years. Generally, the longer the time frame, the higher your short-term fixed interest rate will be. After this time frame has passed, the rate will change each year. While this allows you to take advantage of a lower interest rate in the beginning of your mortgage loan, there is more risk involved later on when the interest rate begins to fluctuate.

Should I Get a 15- or 30-Year Mortgage Term?

Understanding your financial health and plans for the future can help you determine what length of loan would work best for you. While there are many different loan lengths, a 15- or 30-year mortgage loan is most common.

A 15-year loan allows you to pay off your home sooner with higher monthly payments, while 30-year loans offer lower payments for a longer period of time. The downside to 30-year loans is that you’ll be paying significantly more interest than a 15-year loan, even though the overall payment each month is lower.

The flexibility of mortgage types, interest rates, and lengths allows people of all financial backgrounds to find the mortgage loan right for them. However, understanding the details of your legal agreement can help ensure that you make the best and most realistic decision for your future. After all, proper financial planning doesn’t just include monthly payments. It also includes saving up for repairs, accidents, and managing your expenses. But by keeping all these factors in mind, you can set yourself and your family up for success for years to come.

Sources: Federal Trade Commission