Both money market accounts and certificates of deposit (CDs) enable your savings to generate interest. In general, money market accounts offer lower interest rates but more flexibility for withdrawing money. On the other hand, CDs tie your money up for a period of time, but they’ll likely provide a better interest rate.

After you’ve started to save up some money, you’ll likely consider the many options for generating interest on your savings. Though you may have a traditional savings account, you might look to a money market account or a certificate of deposit (CD) as other choices that may suit your situation. But choosing between money market vs. CD can be tough.

While both money market accounts and CDs have some similarities with traditional savings accounts, they often have higher interest rates. This means that your savings will grow faster over time, but it’s good to know both the advantages and disadvantages of these kinds of accounts.

Read on to learn how to choose between a money market account and a CD as well as details about both of these account types.

Choosing Between Money Market Account and CD

When choosing a savings account like a money market account or a CD, it can be helpful to consider the similarities and differences. Additionally, it’s beneficial to think about your particular situation, including your short- and long-term needs.

Use the following chart to help guide you toward a savings account that could work for you.

| Money Market Account vs. CD | ||

|---|---|---|

|

Money Market Account |

CD |

|

|

Flexibility |

Allows for up to six withdrawals per month, enabling short-term investment. | Money is generally tied up for a set period of time, so better as a long-term investment. |

|

Interest Rates |

Usually has a higher interest rate than a traditional savings account, but often lower than a CD. Interest rate may change over time. | Usually has a higher interest rate than most other savings accounts, but lower than stocks. Predictable, fixed interest rate. |

|

Penalties |

Generally no penalties or fees. | May include early withdrawal penalties. |

|

Minimum Balance |

May require a minimum balance of $500 to $25,000 or more. | May require a minimum balance of $500 to $10,000 or more. |

|

Safety |

Backed by FDIC insurance up to $250,000. | Backed by FDIC insurance up to $250,000. |

While that provides a high-level look at both money market accounts and CDs, it can also be useful to take a closer look at both of these account types.

What Is a Money Market Account?

A money market account is a type of savings account that earns interest over time. Like a traditional savings account, a money market account enables you to withdraw money up to six times per month. Some money market accounts even include debit cards for easy withdrawals.

That said, the primary reason to choose a money market account is that it may have a higher interest rate than a traditional savings account. However, this higher interest rate often comes as a result of a required account balance, which can vary anywhere from $500 to $25,000 or more. Also, the interest rate for a money market account may change over time.

Importantly, money market accounts are insured by the Federal Deposit Insurance Corporation (FDIC), which means that your money is backed by the federal government up to $250,000 if the financial institution holding your money were to fail.

Here are the key points to remember when considering a money market account:

- Similar to a savings account: You can withdraw money up to six times per month, often with the convenience of a debit card.

- May have required minimum balance: Your account may require a minimum balance to keep it open.

- Could have a higher interest rate: Higher interest rates help your money grow faster. For instance, on a $10,000 deposit, the difference between a 0.1 percent and 1 percent interest rate is almost $500 after five years.

- Money is FDIC insured: Your account is insured up to $250,000 by the federal government.

While money market accounts offer a flexible way to stash your savings, a CD may offer even higher interest rates — but with less flexibility.

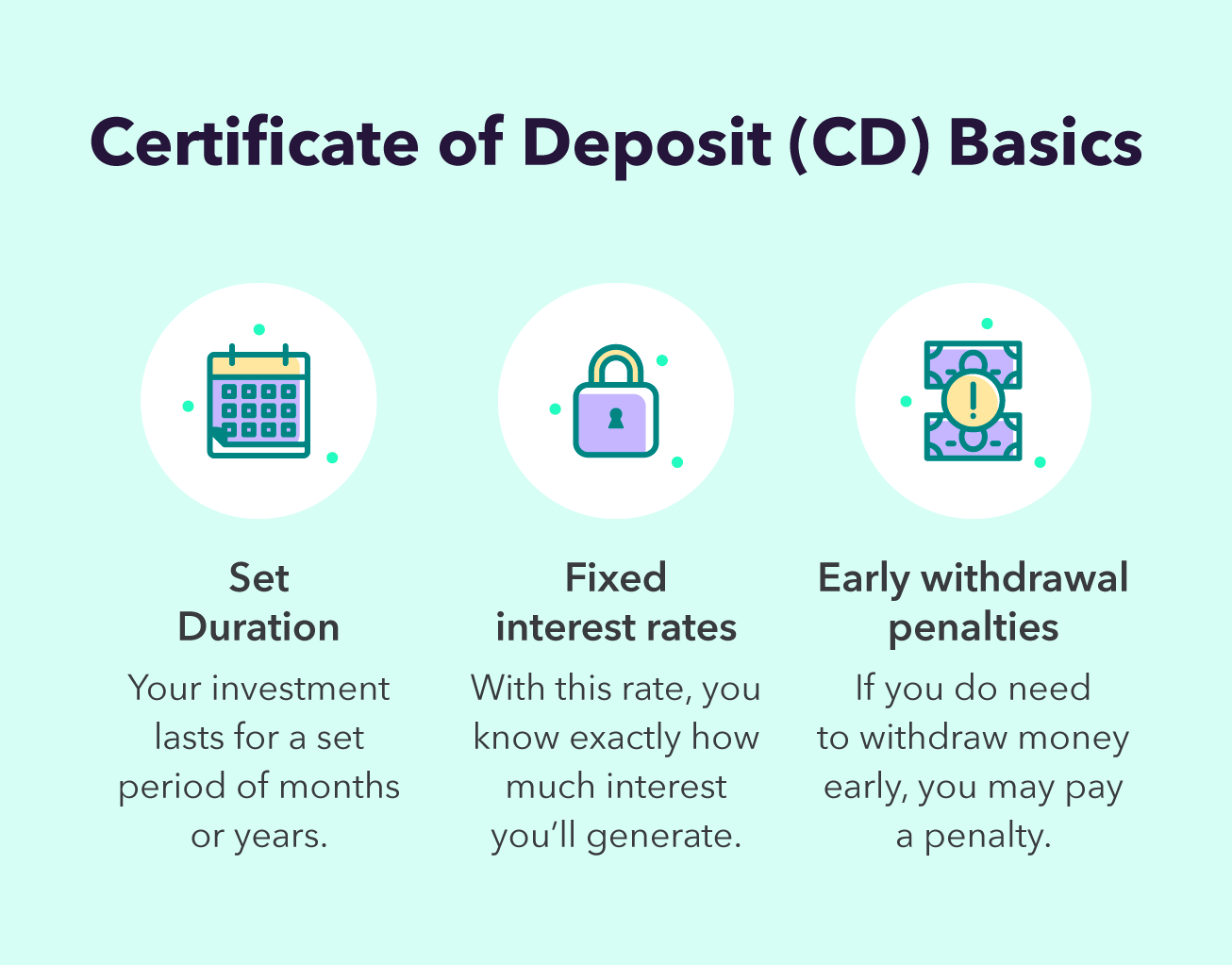

What Is a CD?

A certificate of deposit (CD) is a type of savings account that requires a set deposit for a set period of time. Unlike a traditional savings account, you generally cannot make regular withdrawals from a CD without penalty. Instead, you’ll arrange to have your money returned to you with interest after a predetermined period of time — as short as a few months and up to five years or more.

However, in exchange for a lack of flexibility, CDs often provide higher interest rates than money market accounts. Additionally, the interest rate for a CD is fixed, which means that you can anticipate exactly how much money you’ll make over time by investing in your CD.

Your CD may require a minimum deposit — generally anywhere from $500 to $10,000 — but most CDs don’t have any account fees for their duration. That said, a CD generally involves a penalty for early withdrawals from the account, so you’ll want to be sure that you don’t need access to that money for the entire term.

Like money market accounts, CDs are backed by the FDIC, which means that your investment will be protected by the federal government up to $250,000.

Here is what you should keep in mind about CDs:

- Set duration: A CD has a set duration — usually several months or years.

- May involve penalties for early withdrawals: If you do need access to your money, you can withdraw it, but you may have to forfeit the interest or pay a penalty for doing so.

- Generally have higher interest rates than other savings accounts: Although they are less flexible than other accounts, they generally have higher interest rates. The rates are also usually fixed for the duration of the CD, so you know exactly how much interest you’ll generate.

- Backed by federal insurance: Your investment is protected up to $250,000 by the FDIC, which is part of the federal government.

With all of this knowledge, you’re ready to think about whether a money market account or CD may be right for you.

No matter which account you choose, you’ll be making an excellent decision to help your savings grow with interest over time. In addition to savings accounts, you’ll also want to consider tax-advantaged retirement accounts that allow for long-term saving and potentially larger returns over time.

To continue your saving momentum — or to get started by committing to save each month — it’s important to track all of your accounts to keep a bird’s eye view of your financial picture. Once you’ve got a budget, you’re on the way to reaching your financial goals.