For millions of American homeowners, their mortgage payment is one of their greatest financial commitments. With mortgage rates hitting record lows this year, it’s no wonder that people are interested in the possibility of refinancing their homes.

Instead of only focusing on the potential of saving hundreds per month, it’s essential to fully understand how much it costs to refinance. We wanted to outline the basics so you have a strong starting point in your refinancing decision-making process.

How Much Does It Cost to Refinance a Mortgage?

Mortgage refinancing is defined as replacing your existing mortgage with a new one. There are multiple types of mortgage financing loans that require different considerations, such as cash-out refinances. In any case, working with your mortgage lender is essential to figure out if refinancing will be worth it for you.

Below, we’ve listed the main types of fees you can expect when refinancing your mortgage. Depending on the situation, you could expect to pay anywhere from $5,000 to $10,000 in fees upfront.

The cost of each fee varies greatly based on the type, size, and location of your home. You’ll also have to factor in your credit score and other aspects of your personal financial profile. Also, refinancing fees vary between states and lenders.

| Refinancing Closing Costs | |

|---|---|

| Type of fee | Estimated cost |

| Loan origination fee | 0.5% – 1% of loan amount |

| Appraisal fee | $300 – $400 |

| Credit report fee | $30 – $50 |

| Title insurance fee | $500 – $1,000 |

| Government recording fee | $30 – $50 |

| Property survey cost | $300 – $800 |

| Home inspection cost | $300 – $600 |

| Flood certification cost | $15 – $20 |

| Prepaid Interest Charges | Varies based on the interest rate and when your loan closes |

| Tax service cost | Varies |

| Attorney cost | Varies |

| Mortgage points | One point costs 1% of your mortgage amount |

| Loan reconveyance fee | $50 – $65 |

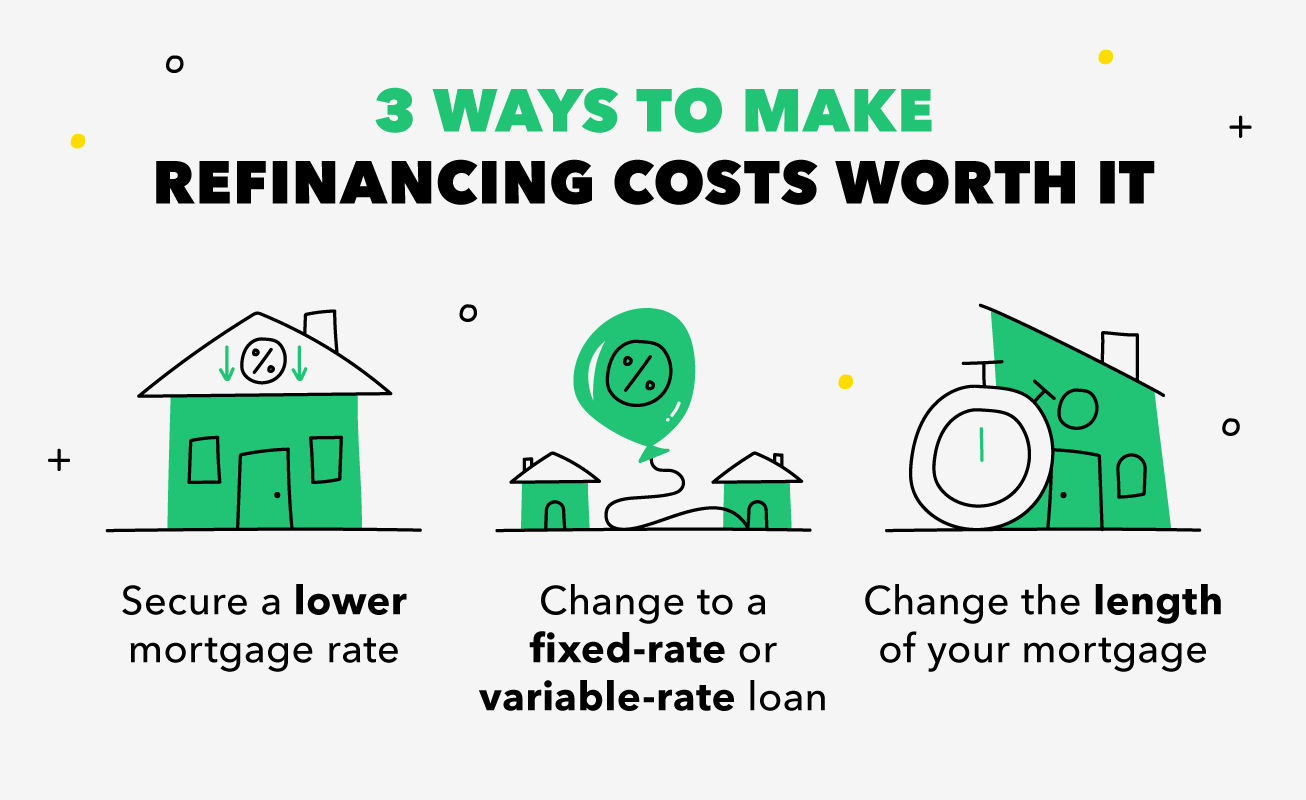

By doing a cost-benefit analysis with your lender, you’ll determine if the short-term financial burden of refinancing is feasible. As with any financial endeavor, you’ll need to do your due diligence.

It’s worth noting that some refinancing costs are tax-deductible based on certain criteria. For example, you can usually receive tax deductions on mortgage interest and closing costs.

Questions to Ask Yourself Before Refinancing

Before you make your decision, examine your long-term goals to see if you can justify the cost to refinance a mortgage. Ask yourself key questions about how much you’ll actually benefit from refinancing your loan or not.

1) Will the Investment Pay for Itself?

Ask yourself how long it will take you to earn back the cost of refinancing your home. Consider your ability to break even in a timely fashion. For example, it makes sense if you’re planning on staying in your home for the long haul and you can break even in a few years. If you might move in a year or two anyway, maybe you should reconsider refinancing.

2) Is Your Loan Seasoned?

Your loan is considered seasoned when it’s been out for at least a year and the borrower has a reliable payment history. If you’re five to ten years into paying off a 30-year mortgage, refinancing might not actually benefit you.

For example, if you’re losing your potential savings to additional interest costs, you’ll likely just lose more by refinancing. On the other hand, refinancing could be a great option if you can ensure you won’t be losing money to interest fees.

3) How Can I Lower my Refinancing Costs?

Focus on improving your credit score and debt-to-income ratio before refinancing your mortgage. You’ll be in a strong position for negotiation to get the best possible rate. It’s worth asking if you can waive the appraisal fee, which could save you hundreds.

If a property has been appraised fairly recently and prices have not significantly changed, your mortgage lender might be able to waive a new appraisal. Also, don’t hesitate to comparison shop to find discounted third-party fees.

Will Refinancing Affect My Credit?

Refinancing a mortgage has the potential to impact your credit score, although not permanently. If refinancing makes sense for your situation, you shouldn’t be concerned about it hurting your credit in the long term. It might not be the most ideal situation, but it’s extremely common and typically relatively easy for your credit score to bounce back.

By consolidating your credit inquiries, you’ll prevent multiple hard inquiries from raising red flags. Also, you can work with your lenders to avoid having them all run your credit, which could risk lowering your credit score.

From a long-term financial planning standpoint, home refinancing can be a smart move. Even if you’re considering refinancing your car loan, it makes sense to look into refinancing your house first. After all, a mortgage refinance allows you to benefit from more cash in your pocket due to lower monthly payments.

Since financing decreases your monthly bills, you’ll want to be strategic about where you direct your additional funds. Are you saving for college tuition, a wedding, or retirement? Are you working towards becoming debt-free? Refinancing is a great time to get serious about budgeting and prioritizing your personal financial goals.

Sources:

Federal Reserve | Interest.com | The Nest | My Mortgage Insider | Freddie Mac