Table of Contents

Having a disability means certain things could be more difficult, but that doesn’t mean financing a home and car has to be. As a person with a disability, having a home and car that suits your needs for accessibility and safety is essential—but where do you start with finding the best options for you?

Luckily, there are many options when it comes to financing a home and car. Below, we’ll outline the process of applying for a home or auto loan as well as provide the additional resources available to you.

Government Definition of a Disability

The federal government defines a person with a disability as someone who:

- Has a physical or mental impairment that substantially limits one or more “major life activities”

- Has a record of such an impairment

- Is regarded as having such an impairment

The Department of Housing and Urban Development (HUD) defines “major life activities” as being walking, speaking, hearing, seeing, breathing, working, learning, performing manual tasks, and caring for oneself. It can also include the operation of major bodily activities.

HUD includes examples of a “physical or mental impairment” being orthopedic, visual, speech and hearing impairments, cerebral palsy, autism, epilepsy, muscular dystrophy, multiple sclerosis, cancer, heart disease, diabetes, HIV, developmental disabilities, mental illness, drug addiction, and diabetes.

These are just a few examples of the many different types of disabilities. Keep in mind that the federal government considers a disability to be any impairment that imposes a substantial limitation on a major life activity. Having a disability that is recognized by the federal government could qualify you for financial assistance and mortgage programs for people with disabilities.

Financing Home Ownership for Those with Disabilities

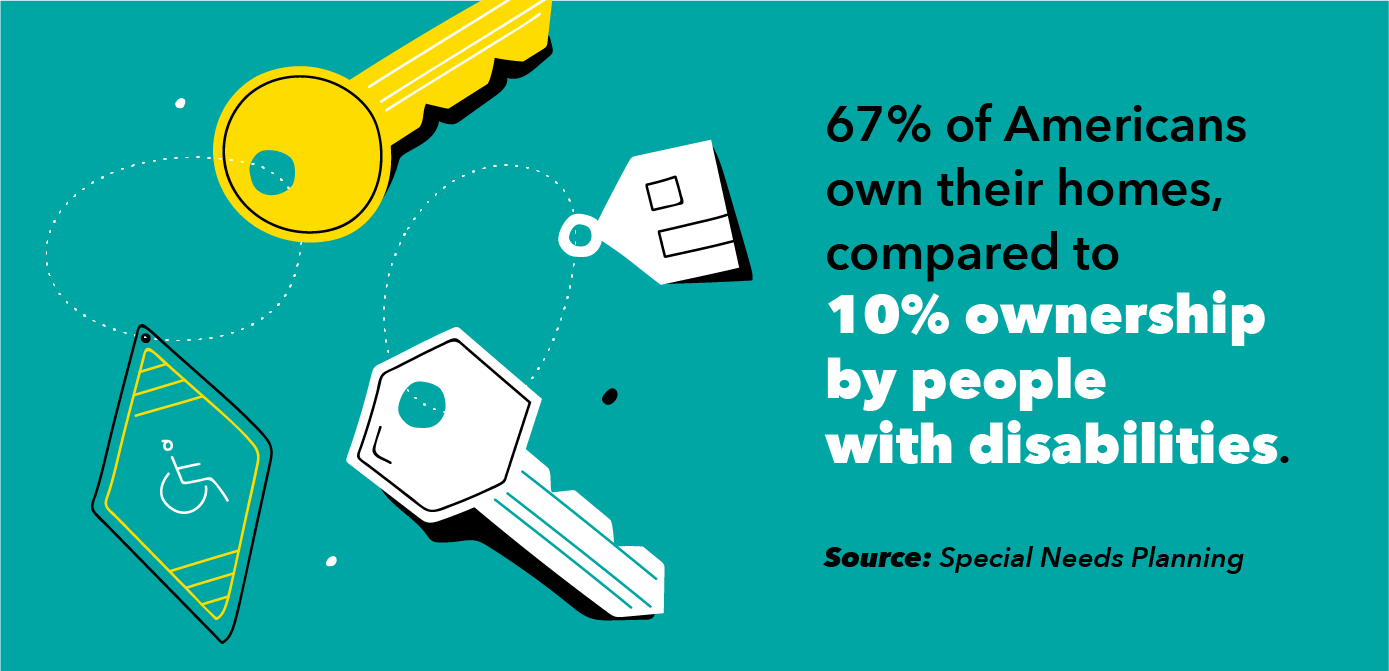

Owning a home with a disability would be especially ideal because you can ensure it has the proper accessibilities that fit your needs. However, owning a home is a huge financial decision that many people resign to be unattainable. Consider median earnings for those with no disability are over $30,469, the median income for individuals living with a disability is $20,250.

Getting a loan for your own home can look daunting no matter your income, so it can be especially so if you’ve struggled with meeting loan income requirements. Thankfully there are several options to choose from if you’ve had difficulty with loan approvals. These programs can assist you in both purchasing a home and outfitting it to accommodate your requirements, as well as help with understanding the basic jargon of home financing.

Fannie Mae

The Federal National Mortgage Association (FNMA, more commonly known as Fannie Mae) is a government-sponsored enterprise founded to make mortgages available to moderate-to-low- income borrowers. They provide affordable housing financing for homebuyers and renters in the U.S, and offer two primary lines of business:

1. Single-Family

Fannie Mae’s single-family business funding makes stable, predictable mortgage financing options like the 30-year, fixed-rate mortgage option a possibility. The lenders they work with can tailor mortgage loans to meet the needs of different borrowers.

2. Multi-Family

The multi-family business funding provides financing options for multi-family rental properties. They work with a national network of participating lenders to help finance apartment buildings across the country.

VA Home Loans for Disabled Veterans

The VA Home Loan is a great option for veterans with disabilities or active duty military who are looking to buy a home. Most veterans who qualify for a VA home loan are eligible for no down payments, low-interest rates, no mortgage insurance premiums, and a host of other benefits.

The VA Loan Entitlement is the actual amount (percentage or dollar) that the VA will guarantee. While the VA Loan Entitlement will vary by individual, the standard Entitlement is either $36,000 or 25% of the total loan amount.

Habitat for Humanity

Habitat for Humanity is a global nonprofit, volunteer-based organization working in communities across the U.S., and in approximately 70 countries. They offer families in need of decent and affordable housing the option to build their own home (alongside volunteers) and pay an affordable mortgage. They also renovate existing homes for those whose accessibility needs are not being met and assist people repair or renovate their own homes or neighborhoods.

Local Habitat for Humanity family selection committees select homeowners based on the following criteria:

- The applicant’s level of need

- Their willingness to partner with Habitat

- Their ability to repay a mortgage through an affordable payment plan

How to Apply for a Mortgage Loan

Once you’ve decided to mortgage a house, it’s time to start applying for a mortgage loan. This process takes a while and has several steps, so it’s important to make sure you know the different aspects of applying and the items you’ll need in order to apply. Finding the best option for you and your disability can take a little longer, so be prepared with a list of questions about financing a home that is accessible for you.

Check Your Credit Score

When applying for a mortgage loan, lenders want to be sure you have a good credit score and a positive history of making payments on time. This proves to them that you’re a trustworthy person to lend money to, as you are more likely to pay it back than someone with a lower credit score.

If you’re wanting to find an accessible home ASAP, check your credit early and ensure you’re in a good place to begin financing a home. If your credit is in a good place, keep doing what you’re doing, but if it needs a little help take action to make sure it’s in a good enough place to qualify you for the loan you need. Whether that’s talking to your credit lender, a banker, or a financial coach, make sure you’re doing what you can to get your credit up to where it needs to be.

Apply with Various Lenders and Find the Right One for You

Finding the right mortgage lender includes much more than having a good credit score. You want to work with a team of professionals, helpful lenders who will guide you through the process. Consider making the process easier, and find better lender options, by getting pre-approved for your mortgage.

To ensure that you find the right lender for your individualized circumstances, shop around and compare rates from the various options. When you’re shopping around, make sure you’re asking questions about their process, fees, and anything else you should know before deciding. Read the fine print on their quotes, and take your time comparing.

Gather Documentation on Debts and Expenses

Once you’ve settled with the best lender for you, it’s time to round up the documentation you’ll need to apply for your mortgage.

Mortgage applications want to know your full financial history. This includes listing all of your debts, and the regular fixed expenses you spend money on every month. This includes everything from car insurance to student loan payments, so be sure you’re reporting those numbers accurately. Save all of your previous bills, like rent and utilities, so you can report those numbers as accurately as possible.

Though you’ll need to report those numbers, you won’t need to submit those bills. Your lender will check those against your credit report, which will list your bills and whether or not you’re paying them back on time.

Even if a debt doesn’t show on your credit report, you are still obligated to disclose it on your application as intentionally misrepresenting assets constitutes fraud.

If you have no previous credit history, be prepared to give your lender a list of previous landlords and utility providers so they can check your history of on-time payments.

Provide Proof of Income

Next, you’ll need to establish that you can afford the payments on the loan you’re applying for. Depending on your type of income, you may need to prove:

Employment income

Lenders will ask for your W-2s from the last two years as well as your individual pay stubs showing your income from the past 30 days. If you have multiple jobs, bring the necessary paperwork from all of your jobs.

Lenders will also likely ask for signed copies of your tax returns from the past two years and will ask you to fill out forms allowing them to request copies of those forms directly from the Internal Revenue Service.

Unemployment income

If you’re employed in a seasonal sector that includes regular layoffs—such as tourism, agriculture, or fishing—your insurance payments from unemployment can count towards your regular income.

You will have to prove that you’ve worked in these seasonal fields for the past two years, and the lender will ask your employer if you will be rehired next season. Bring in your checks that show year-to-date earnings, or a photocopy of your bank statement showing the deposit.

Disability income

Disability income counts as qualifying proof of income. Lenders will ask for a copy of your disability policy or the benefits statement from the source of your disability income, showing your eligibility and the amount of and frequency of payments. If your disability comes from the Social Security Administration, you will need your SSA award letter or current receipt.

Under policies instituted by the Consumer Financial Protection Bureau, lenders cannot ask doctors for details of your medical condition. They should assume that disability payments will continue for the foreseeable future unless your paperwork indicates otherwise.

Other income

If you make any other type of income that isn’t included in this list (pension, a car allowance, Social Security, annual bonus, royalties from published works) you can count it as income if you can document it and prove it as your own.

The general rule toward these outside sources of income is that you must prove it was a regular, steady source of income for the last 12 months, and that you can expect to continue receiving it for at least the next three years.

To prove ownership, use letters or statements spelling out what you’re entitled to as well as check stubs or photocopies of bank statements showing the actual deposits.

Assets

If you own CDs, savings accounts, retirement accounts, stocks or bonds, or a life insurance policy with cash or real estate value, you will need to provide proof of ownership and market value.

You will need deeds and other documentation for real estate, and most lenders will accept your two most recent statements from a bank or brokerage firm to prove ownership of stocks, bonds, and other monetary holdings.

Tips for Auto Loans for Individuals with Disabilities

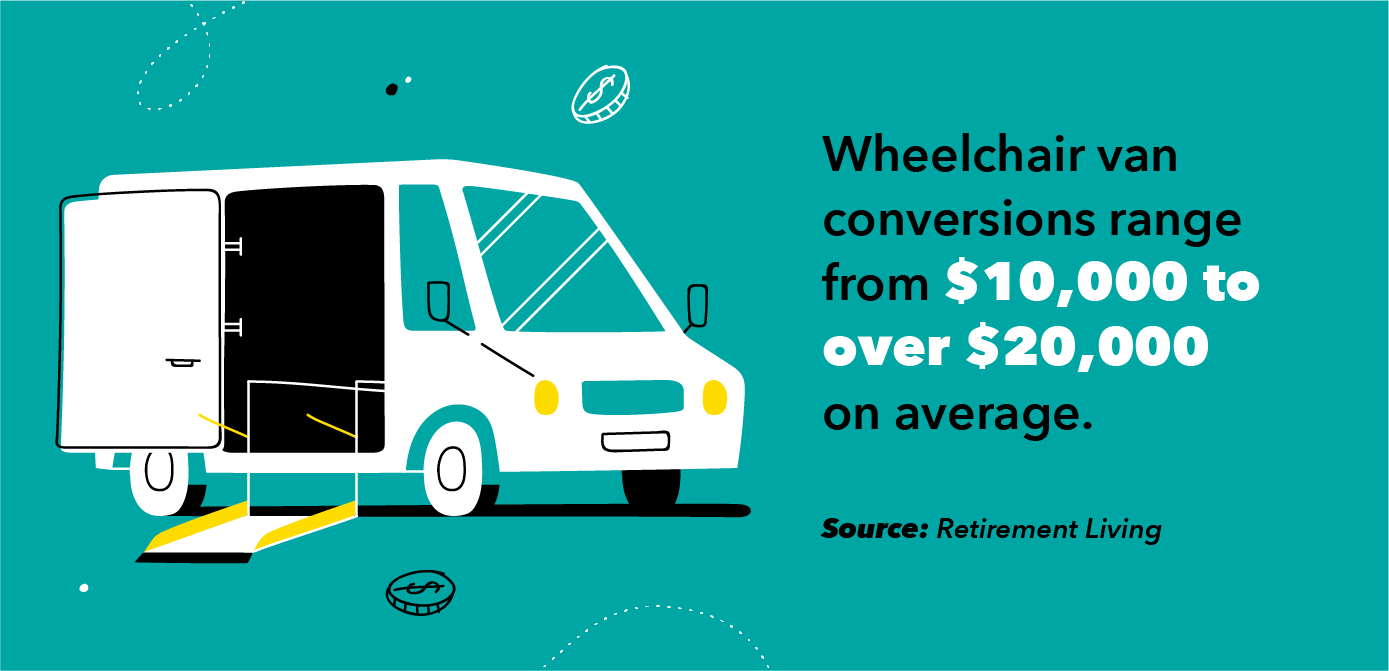

Just like with finding a loan to finance your home, finding a car to accommodate your disability is vital to ensuring you have the means to transport yourself. In most cases, making a car accessible means buying the car at cost, and then making conversions and additions to outfit it to your requirements. While choosing the best auto loan and lender to finance your car can take a lot of work, there are clear steps you can take to make the process as seamless as possible.

Check Your Credit Score Ahead of Time

Similar to applying for a mortgage, lenders will want to make sure you have good credit. Look at your credit score months before you apply for a loan to make sure you’re in good standing. If your credit isn’t looking good enough to qualify you for a loan, consider making some larger payments to pay off more of your debt, or talk to your credit lender for advice on how to improve your score before you apply for the loan.

Consider Getting a Co-Signer

If you’re worried that your credit score alone won’t allow you to qualify for an auto loan, consider asking someone to be your co-signer. Having a co-signer essentially means you are asking someone to help you take on the responsibility for repaying the loan, meaning they serve as an additional payment source if you can’t repay the loan in full yourself. They are not responsible for monthly payments and can help you qualify for a loan by combining your credit and theirs. This is a big responsibility to ask of someone, as it puts their credit at risk if you don’t repay. Keeping all of that in mind, think critically of who would be willing to help you qualify by co-signing for a loan with you.

Save for a Larger Down Payment

Sometimes it will help you pay off an auto loan faster by signing up for a larger down payment, resulting in smaller monthly payments. Do your research on a down payment that might help you pay off your loan faster, but still reasonably fits in your budget, and start saving up for it. When shopping for your car, make sure to ask your dealer what their payment options are with a larger down payment.

Additional Resources

Sources

Self | Department of Housing and Urban Development | VA Home Loan Centers | Fannie Mae | Interest.com | Consumer Finance | Investopedia |