There you are, sitting in your high school’s guidance office talking with your counselor about heading off to college after graduation. You’re all excited thinking about the new friends and freedom you’ll have until you go home to parents who remind you that college isn’t cheap. With over half of college students taking on debt, there’s a chance you may have to take out a student loan to pay for room, board, tuition, and books.

When it comes to the type of loan a student takes out, they will often take out federal student loans, as they’re usually cheaper than private loans. And, if you do take out FedLoans, there’s a high chance your servicer is FedLoan Servicing, as they provide roughly a third of services to all federal student loan recipients. Operated by the Pennsylvania Higher Education Assistance Agency (PHEAA), FedLoan Servicing is one of the nine federal loan providers.

Confused? Don’t fret. We’ll go over all you need to know about FedLoan Servicing, benefits and services, repayment plans, student loans explained, and more. For a full understanding of what FedLoan Servicing is, continue reading. Or, if you’re looking for an answer to a specific question, navigate using the links below.

What is Student Loan Servicing?

When you finish filing with FAFSA to determine how much federal aid you qualify for, the Department of Education will assign you a loan servicer. A student loan servicer, such as FedLoan Servicing, can help you manage your account and repay your loans once you’ve graduated or stopped attending college. After this point, your loan provider will bill you and collect your payments.

Student loan servicers also provide assistance with other situations as well, such as creating repayment plans, which will be discussed later, and can provide help on consolidating multiple loans and deferring loans.

How Do I Determine My Loan Servicer?

When you apply for student loans from the federal government, you may think you have to repay the Department of Education directly. Instead, the Department of Education gets help from a total of nine federal loan servicers, including:

- FedLoan Servicing

- Navient

- Nelnet

- Great Lakes Educational Loan Services, Inc.

- MOHELA

- HESC / EdFinancial

- CornerStone

- Granite State – GSMR

- OSLA Servicing

When you receive federal aid, you don’t get to choose your loan provider. Instead, the Department of Education will assign one to you. This may make knowing who your loan servicer is difficult because you didn’t get to pick your servicer yourself. Usually, when you do get assigned a federal loan lender, they will send you an email once they are assigned to your account. But, if you thought it was spam or simply ignored the email and it’s lost in your inbox filled with thousands of unread messages, you may not know who your loan servicer is.

To determine who your loan servicer is, you can check on the National Student Loan Data System website. Once you’re on the NSLDS website, click “Financial Aid Review” in the left-hand column, log in with your FSA ID or create one, and look at your information to determine who your loan servicer is.

What is a FedLoan and What is FedLoan Servicing?

If you determined who your loan servicer is and found out it was FedLoan Servicing, you may be wondering who they are. FedLoan Servicing is one of the loan servicers contracted by the Department of Education. As of June 31, 2019, FedLoan Servicing is the largest fed loan provider, shelling out $358.6 billion to 7.91 million students. To access your FedLoan student loans, you can log in to your account on myfedloan.org.

Of the nine fed student loan servicing companies, FedLoan Servicing is the only servicer used for the government’s Public Service Loan Forgiveness Program and TEACH grant program.

- The Public Service Loan Forgiveness Program grants loan forgiveness to eligible public service employees, such as those employed by the government or a non-profit organization. Basic guidelines require you to make 120 qualifying payments under a designated repayment plan while working for an eligible employer.

- A TEACH Grant can help people pay for college if they intend to become a teacher in a high-need field located in a low-income area. To qualify for a TEACH Grant, you must take certain classes and hold a specific type of job to prevent the grant from turning into a loan.

FedLoan Benefits and Services

When you’re stuck with paying student loans after graduation, you may feel overwhelmed and stressed, wondering how you’re going to pay back all of that money. After all, the average student in 2018 graduated college with $31,172 in debt. That’s enough money to buy a brand-new car or put a substantial down payment on a home!

To help you with your repayment, FedLoan Services offers a variety of benefits and services to help you out. These resources include:

- Consolidation Quiz: This quiz can help you determine whether consolidating your fed loans is the right decision for your situation.

- In-school Interest Savings Calculator: Before you graduate, you can take this quiz to see how much money you can potentially save by paying off your accumulated interest before your loan enters repayment.

- Grace Period Interest Savings Calculator: If you have a federal Stafford loan, it will enter a 6-month grace period after you graduate where you don’t have to make payments. However, interest still accrues during these months. Use this calculator to see how much money you can save by making monthly payments.

- Teacher Loan Forgiveness Quiz: If you’re a teacher, you may be eligible for loan forgiveness—this quiz can help you determine if you qualify.

- Frequently Asked Questions: If you have any questions about your student loans, you can scroll through the site’s frequently asked questions to find the answer you’re looking for.

- Student Loans 101: Understanding all there is to know about the world of student loans can be a headache, which is why FedLoan Services created Student Loans 101 to teach you the important aspects of fed loans.

- Interactive Samples for Understanding Your Correspondence: If you’re confused about an email or letter you received in the mail, you can use interactive samples to learn about the components on a variety of notices, such as monthly bills, direct debit bills, interest notices, or loan verification letters.

- Videos: You have access to a collection of videos, ranging from information for service members to IDR plans.

- Online-Chatting, Calling, and Email Support: If the site’s vast collection of resources don’t answer any questions, comments, or concerns, you can reach out to them through their online chat, or by calling or emailing them.

- Mobile App for iOS and Android: For easy access and payments on the go, you can download the FedLoan Student Loans app on your iPhone or Android.

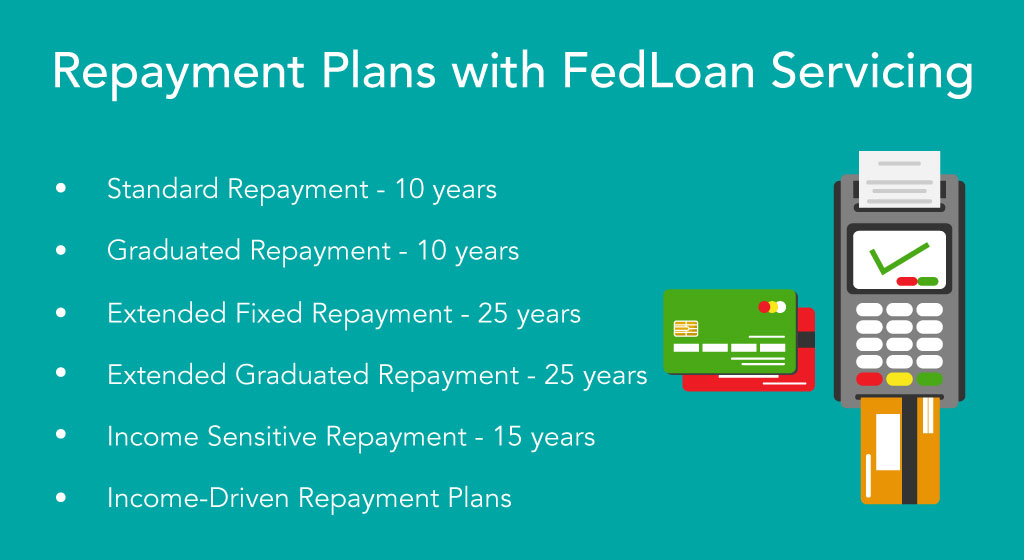

Repayment Plans with FedLoan Servicing

The most important question you’re probably asking yourself is how to repay your loans. Each federal loan servicing company offers student loan repayment plans to choose from. FedLoan Servicing offers a variety of repayment options, so you can choose the one that best fits your financial situation after college.

The repayment plans offered by FedLoan Servicing include:

- Standard Repayment: When you graduate college, you will automatically be enrolled in the Standard Repayment plan, unless you choose another one during your exit counseling. This plan has the quickest payoff with fixed monthly payments over the course of 10 years.

- Graduated Repayment: If you land a job and expect your salary to increase over time, you may want to choose the Graduated Repayment plan. This plan also has the quickest payoff, only taking 10 years, and has lower monthly payments that increase over time, every two years.

- Extended Fixed Repayment: If you left college with a lot of debt, and the previous two repayment plans seem impossible to keep up with, you can choose an Extended Fixed Repayment. With this plan, your term limit is extended, up to 25 years, and can give you a lower monthly payment, compared to the monthly payments the 10-year Standard Repayment plan has. There are fixed monthly payments, and you must have more than $30,000 in outstanding Direct Loans or FFEL Program Loans.

- Extended Graduated Repayment: This plan works the same way as the Graduated Repayment plan; however, similar to the Extended Fixed Repayment Plan, the term limit is extended, up to 25 years. If you hope to be able to pay more money in the future, due to a more lucrative job or a salary increase, this plan will give you lower monthly payments that increase over time. To qualify, you’ll need more than $30,000 in outstanding Direct Loans or FFEL Program Loans.

- Income Sensitive Repayment: If you’re concerned your monthly payments are too high, you need short-term relief, and your loans don’t qualify for a more beneficial repayment plan, the Income Sensitive Repayment plan can help. This plan extends the repayment period up to 5 years (a total of 15 years), giving you lower monthly payments because they’re stretched out over a longer period of time. Additionally, this plan’s monthly payments are based on your monthly gross income, and must at least cover the interest accrued on the loan(s) every month. The only loans eligible for this plan are those disbursed in the FFEL Program.

- Repayment Plans Based on Your Income: Income-Driven Repayment (IRD) Plans are based on a variety of factors, including your income, the state you live in, and your family size. Because these factors can change, you must provide an annual update, so your payments match your current situation. If you don’t recertify every year, your monthly installment amount may increase, or your interest may be added to your principal balance. These plans are suitable for those who don’t have an income, have a large amount of debt, or are unsure whether they can afford their monthly payments.

There are four IRD Plans to choose from, including: - PAYE: The Pay As You Earn (PAYE) plan uses your income and family size to determine your reduced monthly payments, usually 10% of your income, which are paid off for up to 20 years. After 20 years of qualifying payments, the remaining balance may be eligible for forgiveness.

- IBR: The Income-Based Repayment (IBR) plan uses your income and family size to determine your reduced monthly payments, usually 15% of your income, which are paid off for up to 25 years. After 25 years of qualifying payments, the remaining balance may be eligible for forgiveness.

- ICR: The Income-Contingent Repayment (ICR) plan uses your income, family size, and the total amount of eligible loan debt to determine your reduced monthly payments, which are adjusted based on the lesser of (1) 20% of your discretionary income, or (2) the amount you would pay under a fixed repayment plan over the course of 12 years. Payments under this plan are made for up to 25 years, with loan forgiveness after 25 years of qualifying payments.

- REPAYE: The Revised Pay As You Earn (REPAYE) plan offers reduced monthly payments after calculating your and your spouse’s income, if applicable. Monthly payments are usually 10% of your income, which are paid off up to 20 years, or 25 years for graduate and professional study students who took out Direct Loans. After 20 years (or 25 years for graduate and professional study students) of qualifying payments, the remaining balance may be eligible for forgiveness.

Along with FedLoan Servicing repayment plan options, there are a few other ways you can pay back your fed loans. These options include:

- Consolidation: If you have to make multiple monthly payments because you have federal loans from multiple fed student loan servicing companies, you can consolidate your loans, or combine them, so you only have to make a single monthly payment. Loan consolidation may also lower your monthly payment and give you a more extended period of time, up to 30 years, to repay your loans. However, because your loan is extended, you might have to pay more money in interest.

- Deferment or Forbearance: If you’re in a situation where you can’t keep up with your monthly payments, you can work with your loan servicer to apply for a deferment or forbearance. These options will temporarily stop collecting monthly payments or will reduce your monthly payments. The major difference between the two is that with deferment, you may not have to pay the interest that accrues on certain types of loans during the deferment period, while with forbearance, you will have to pay the interest that accrues on your federal student loans.

Paying off student loans can be difficult for some people, depending on their financial situation. Luckily, there’s been an increase in the number of employers who offer student loan assistance programs, where they’ll help pay off some or all of your loans. However, not every employer offers this benefit, so if you’re still struggling to repay your student loans, you can seek the help of a student loan expert for assistance.

Common Problems with FedLoan Servicing

As with most things in life, it’s hard to be perfect. While FedLoan Servicing offers great benefits and services, as well as a variety of repayment options to choose from, there are some areas for improvement. Some of the most common complaints with FedLoan Servicing, according to a survey conducted by Student Loan Planner, include:

- Poor payment handling: One common complaint with FedLoan Servicing is how they handle making payments. In some cases, payments weren’t processed accurately, leading to incorrect balances.

- Poor handling of the Public Service Loan Forgiveness program: As mentioned earlier, the PSLF program can offer forgiveness to public service workers who make 120 qualifying payments. A common problem with FedLoan Servicing is that it’s very difficult for public service workers to receive forgiveness. In fact, of the 110,729 applicants as of June 30, 2019, only 1,216 applications were approved, with only 845 unique borrows actually having their loans dismissed. That means 99.3 percent of PSLF applicants were denied forgiveness.

- Customer service problems: Major frustrations with FedLoan Servicing have to do with their customer service. According to this study, many customers claimed their representatives were “incompetent,” and “unhelpful.”

- Not receiving enough information about loans: Lastly, fed loan borrowers claimed they didn’t receive enough information about loans, especially when it came to Income-Driven Repayment plans. Many borrowers said they didn’t know how the repayment plans worked, and representatives were lousy in giving them adequate information.

How to Submit a Complaint to FedLoan Servicing

Navigating the world of student loans is difficult, and if you ended up with a bad experience with FedLoan Servicing, it’s important that your voice is heard. There are a variety of ways you can submit a complaint to FedLoan Servicing, such as:

- Better Business Bureau: Although FedLoan Servicing isn’t BBB accredited, you can still file a complaint through their website. The BBB works to help consumers solve their problems with companies, and will forward your message to FedLoan Servicing, or any business you file a complaint against, and ask for a response within 14 days.

- Federal Student Aid’s Feedback System: The FSA, powered by the Department of Education, created a system where borrowers can supply feedback, such as a complaint or a positive experience regarding your loans, as well as upload supporting documents and files. You can also report suspicious activity, such as a potential scam. ed.gov warns against scams, such as fraudsters trying to take your money by posing as a fed loan servicer officer.

- Consumer Financial Protection Bureau: You can also submit a complaint with the CFPB by answering a few questions, such as the problem you’re having, the company you’re filing a claim about, and the people involved.

How to Change Your Student Loan Servicer

Unfortunately, there aren’t too many ways you can change your student loan servicer. Typically when you receive aid from a federal student loan servicing company, you’re stuck with them. There are, however, two ways you can change your student loan servicer:

- Consolidate your loans: As mentioned previously, if you have loans from more than one federal loan servicing company, you can consolidate your loans so you can make one payment instead of multiple. When you consolidate your loans, you can choose one of the loan providers you’re borrowing from, such as FedLoan Servicing or Great Lakes Educational Loan Services, Inc. However, it’s important to remember that only FedLoan Servicing offers TEACH Grants and Public Service Loan Forgiveness. If you’re confident you might not qualify for one of these programs, switching to another loan servicer may be a better move.

- Refinance your loans: The second option to change your student loan servicer is by refinancing your loans. Refinancing means you transfer your current student loans to a private lender, such as a bank or credit union. The advantage of refinancing is that most private lenders may give you a lower interest rate and may have better customer service. However, a significant disadvantage is that once you refinance, you can never go back to your fed student loan servicer. This means you will no longer be eligible for forgiveness and will not have access to any of your federal student loan lender’s benefits.

FedLoan Servicing Contact Information

If you need to reach out to FedLoan Servicing, you can create a secure online account on the FedLoan student loans website and send an email. You can also call or fax FedLoan Servicing with these numbers:

- Call the toll-free number 800.699.2908 Monday through Friday from 8:00 AM to 9:00 PM Eastern Time

- International callers can dial 720.1985 Monday through Friday from 8:00 AM to 9:00 PM Eastern Time

- Hearing and speech-impaired callers can dial the TTY number 711 Monday through Friday from 8:00 AM to 9:00 PM Eastern Time

- The fax number for returning or verifying documentation is 720.1628

Lastly, you can send mail to FedLoan Servicing. However, they have a few addresses, so make sure you send your correspondence to the right one.

Send your payments to:

Department of Education

FedLoan Servicing

P.O. Box 790234

St Louis, MO 63179-0234Completed Direct Debit application forms can be sent to:

FedLoan Servicing

P.O. Box 3661

Harrisburg, PA 17105-3661All letters and correspondence can be sent to:

FedLoan Servicing

P.O. Box 69184

Harrisburg, PA 17106-9184Credit disputes can be sent to:

FedLoan Servicing Credit

P.O. Box 60610

Harrisburg, PA 17106-0610Letters and correspondence related to consolidation can be sent to:

FedLoan Consolidation Department

P.O. Box 69186

Harrisburg, PA 17106-9186The Office of Consumer Advocacy can be contacted at:

Pennsylvania Higher Education Assistance Agency

The Office of Consumer Advocacy

1200 North 7th Street

Harrisburg, PA 17102If you have a different fed student loan servicing company other than FedLoan Servicing, you can find contact numbers on Studentloans.gov.

Key Takeaways on FedLoan Servicing

- FedLoan Servicing is a student loan provider owned by the Pennsylvania Higher Education Assistance Agency, a student aid organization, and is the largest federal loan servicing company.

- When you apply for federal aid, the Department of Education will assign you a fed student loan servicing company, such as FedLoan Servicing.

- FedLoan Servicing is the only fed loan provider with the TEACH Grant and Public Service Loan Forgiveness Programs.

- There are six repayment plans you can choose to pay back your fed loans, including the Standard Repayment, Graduated Repayment, Extended Fixed Repayment, Extended Graduated Repayment, Income-Sensitive, and Income-Driven Repayment plans.

- While FedLoan Servicing has many benefits, common complaints include poor customer service and difficulty receiving enough information on various loan repayment plans.

- You can change your student loan provider by either consolidating your loans or refinancing.