Earnest money is a deposit a potential homebuyer places to signal to the seller that they have serious interest in a property. Also called a “good faith” deposit, this money benefits both the buyer and the seller during the homebuying process.

Purchasing a home involves a number of financial transactions, like saving for a down payment, securing a loan, and paying closing costs. Earnest money is another cost associated with buying a home, but it has the added role of protecting both buyers and sellers from some of the risks associated with a real estate transaction.

- If the purchase falls through, earnest money helps sellers recoup time lost when the house was off the market.

- If the contract terms are not met, earnest money is often refunded to the buyer.

- If the purchase is successful, the earnest money deposit is applied toward the down payment for the home.

Read on to learn all about how earnest money works, how it benefits buyers and sellers, and what these deposits look like in different situations.

How Earnest Money Works

When a buyer is serious about purchasing a property, they use earnest money to signal their intent to purchase it. Although the deal is not finalized at this point, a significant earnest money deposit often prompts the seller to accept an offer, which changes the listing status to “under contract.”

While the amount of earnest money required varies, it frequently amounts to 1 to 3 percent of the total cost of the home. While earnest money is not always required, most sellers do prefer the deposit as a way of finding serious offers, and in competitive markets, a larger deposit provides the possibility of standing out in a crowded field of offers.

When a buyer places an earnest money deposit, the money goes into an escrow account, which means that a third party keeps the funds safe until an agreement is reached. After the house is closed on, the money is applied toward the down payment.

However, the real value of earnest money comes from the way it benefits both homebuyers and sellers.

When Is Earnest Money Refunded?

Earnest money deposits can be refunded in situations that don’t go according to plan, helping to protect homebuyers from several risks.

After the deposit is placed, a buyer and seller enter into a contract to begin the process of changing ownership. This contract describes several contingencies, which are conditions that have to be met before the contract is considered binding.

If any of these conditions are not met, then the contract falls through — and in several cases, the buyer will get their earnest money deposit refunded.

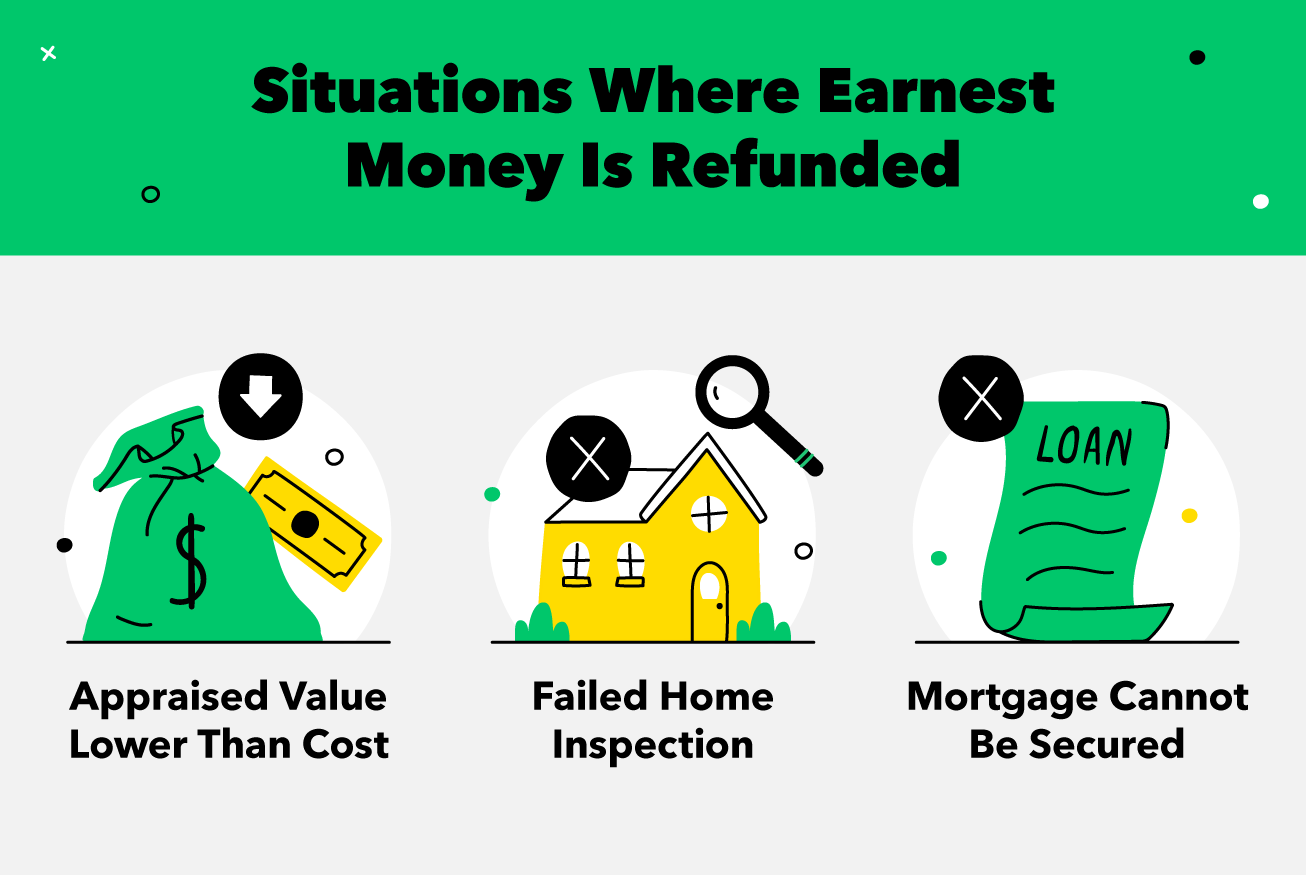

In the following situations, a homebuyer will have their earnest money refunded:

- If the appraised value of the home is lower than the cost to purchase, the buyer can back out of the sale with their deposit.

- If the home fails inspection, the buyer can leave the sale with their deposit or negotiate a lower price based on the cost of repairs.

- If the buyer cannot secure a mortgage for the cost of the home, they are able to void the contract and reclaim their deposit.

That said, all of these situations are only covered if these contingencies are specifically laid out in the contract, so make sure to read carefully before signing. In any case, it’s very helpful for homebuyers to know that their deposit can be refunded in situations where the contract cannot be fulfilled by the seller.

Earnest money deposits also benefit sellers, who take on a risk when they begin contract negotiations with a buyer.

How Earnest Money Benefits Sellers

The most obvious way that earnest money benefits sellers is that it provides a clear signal about which buyers are serious. That said, there is an even more crucial way that earnest money deposits protect sellers during the course of a real estate sale.

After a potential buyer has put down an acceptable earnest money deposit, the seller will typically enter into negotiations. As a result, the listing for the home changes to “under contract,” which discourages other potential buyers.

If the buyer backs out of the sale, the seller has lost time that the house could have been shown to other buyers, and they may need to pay additional costs to re-list the house on the market. However, because the seller is given the earnest money deposit in this situation, they are able to recoup some of their losses.

While these deposits may at first seem burdensome, ultimately they are beneficial to everyone involved in the process of buying or selling a home.

Examples of Earnest Money Deposits

In order to truly understand how earnest money works, it can be helpful to imagine some of the main scenarios that occur after a deposit is placed.

After a buyer puts down an earnest money deposit and contract negotiations begin, there are three typical situations:

- The buyer backs out: If the buyer backs out of the sale, the seller retains the earnest money deposit.

- The contract conditions are not met: Conditions that are not met — like the home inspection contingency or the appraisal contingency — lead to a void contract, so the buyer can walk away with their earnest money.

- The sale closes: If the buyer and seller agree to terms and the sale closes, the buyer’s earnest money deposit is applied toward the down payment.

As you can see, earnest money deposits are positive for both buyers and sellers. Sellers benefit because buyers are more committed and financially invested, and buyers benefit because contingencies allow them to walk away from a situation that was not as it appeared. And if the sale closes, the earnest money is applied to the cost, leaving all parties satisfied.

Purchasing a home is an important financial milestone, and understanding earnest money is a great first step in the process of buying real estate. To make sure you’re on track, fine-tune your budget before preparing to buy a home. And once you’ve settled on the right place, don’t forget to consider additional costs like home improvements or home repairs.